[ad_1]

In a brand new paper, we present that greater than half of the revenue generated by carefully held companies (that’s, companies apart from firms) goes untaxed. Addressing this hole might yield substantial income positive factors along with permitting policymakers to tax the rich extra successfully, a continuously repeated although thus far usually elusive objective.

A pure revenue tax would tax all revenue. Whereas that preferrred doesn’t exist within the US income system, it’s helpful to know why a lot enterprise revenue is untaxed in addition to the income and distributional results of taxing that revenue.

In a separate paper, we describe how we estimate revenue tax liabilities with the public-use Survey of Shopper Funds (SCF) micro knowledge together with the Nationwide Bureau of Financial Analysis’s TAXSIM mannequin. Tax knowledge alone are inadequate to completely perceive these points as a result of the revenue reported on tax kinds already is lowered by legal guidelines, avoidance methods, and noncompliance.

We discovered that whereas the revenue companies report within the SCF is almost the identical as what’s reported within the Nationwide Revenue and Product Accounts (NIPA), each are almost twice what companies report back to the IRS. We consider that SCF respondents disclose how a lot their companies truly earned, whereas the revenue taxpayers report back to the IRS can embrace substantial paper losses even when a enterprise generates earnings for its house owners. Given this speculation, we ask “what if we might tax that revenue?”

To check this concept, we first cut back by half the enterprise revenue reported by house owners with optimistic revenue within the SCF. It is a easy strategy to approximate the actual fact solely about half of all carefully held NIPA enterprise revenue exhibits up on tax kinds. If wealthier enterprise house owners are extra probably to make use of loss-generating enterprise accounting practices, our strategy understates the income and distributional results of taxing all revenue.

Our conclusion: Enterprise house owners would pay way more in taxes primarily based on their SCF+TAXSIM revenue earlier than the 50 p.c shave than they’ve paid as mirrored in SOI values. Many of the increased unadjusted SCF+TAXSIM revenue is because of better enterprise incomes.

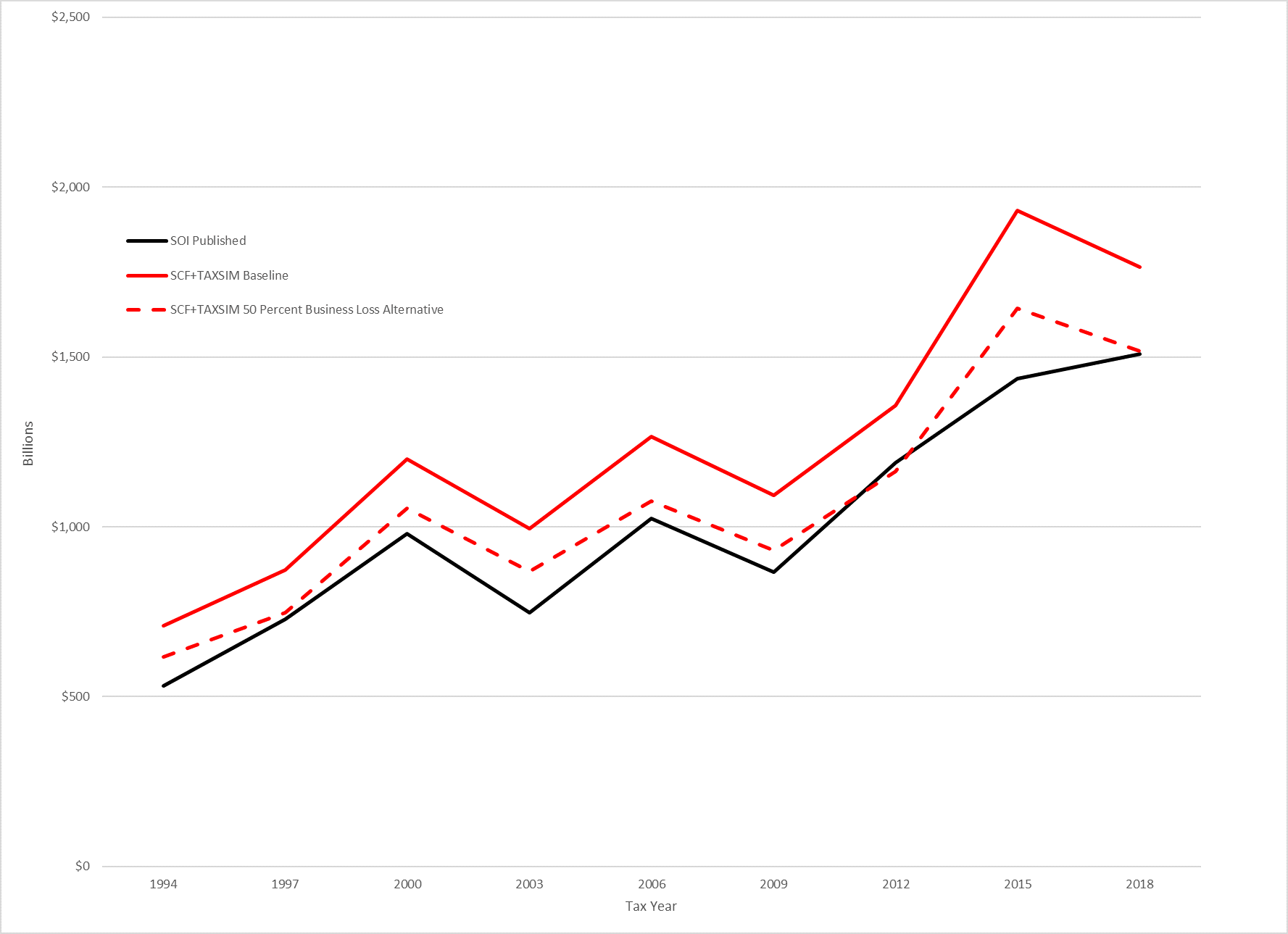

The gaps between SCF+TAXSIM and precise SOI tax liabilities are comparatively secure over time, which is in step with a scientific reporting distinction. Reducing enterprise revenue by 50 p.c carefully aligns the SCF+TAXSIM combination tax liabilities with the revealed IRS knowledge.

As a result of the SCF is a comparatively small pattern, its knowledge are unstable from year-to-year. Nonetheless, the lowered enterprise revenue simulation aligns nicely with revealed SOI over our pattern interval.

We additionally discovered that the distribution of adjusted gross revenue within the SCF extra carefully matches revealed IRS after we cut back enterprise revenue by half.

Determine 1. Mixture Tax Legal responsibility After Credit, SOI and SCF+TAXSIM

Our unadjusted SCF+TAXSIM simulation additionally exhibits a major distinction within the distribution of tax legal responsibility. Households with wealth of $10 million or extra account for 30.3 p.c of taxes in SCF+TAXSIM in comparison with 27.6 p.c primarily based on SOI knowledge. Their common tax legal responsibility jumps by 28 p.c, from $287,830 to $367,145 for these households.

Discovering a strategy to tax what enterprise house owners successfully earn, somewhat than what they report back to the IRS, would have necessary income and distributional implications. And it might be the important thing to extra successfully taxing the rich, an concept that has attracted important consideration amongst policymakers.

[ad_2]

Source link

{kind=link}