[ad_1]

In the event you’ve simply acquired your annual bonus or have financial savings that you just received’t be utilizing within the close to time period, leaving it in your financial institution won’t be such a good suggestion anymore, particularly as inflation continues to creep upwards. Listed here are some options you’ll be able to take into account as an alternative.

Even for these of us who’re ready to withstand way of life inflation (i.e. spending extra as your revenue goes up), we’re not resistant to the results of financial inflation. However what’s extra worrying is that the latest data for Singapore showed our headline inflation has not only been creeping upwards, but is almost at the highest in the last decade.

Not solely are meals costs and transport fares going up, however typically, virtually every part is costlier right now than earlier than. The identical goes for greater oil and gasoline costs (which have gone up much more as a result of Russia-Ukraine disaster) and pandemic-related provide chain disruptions akin to port closures, international commodity costs have been on the rise as properly.

As a way to counter the creeping inflation and guarantee worth stability within the medium time period, the Financial Authority of Singapore (MAS) acted to additional tighten its monetary policy earlier this 12 months (forward of schedule). However will or not it’s sufficient?

Why is inflation unhealthy for savers?

Think about you may have $10,000 in your financial institution financial savings account which pays you 1% curiosity each year which suggests after a 12 months, you should have $10,100. But when inflation is working at 4%, you’ll have wanted to generate $400 of curiosity on this identical capital with the intention to keep the identical shopping for energy that you just began with.

Therefore, though you “earned” $100 out of your financial savings, you may have a poorer shopping for energy now. That’s what we imply after we say your financial savings get eroded by inflation.

Sidenote: As a substitute of 1%, Singapore’s banks are inclined to pay simply 0.05% on most financial savings accounts, together with in your Supplementary Retirement Scheme (SRS) funds.

Now, should you’re about to retire in a number of years time, because of this you successfully have “much less” on your retirement – especially with even basic food prices rising. And if inflation persists or goes even greater, your cash will get you much less meals / transport / dwelling necessities as every year passes. Therefore, the chance of you not having sufficient to dwell on turns into an increasing number of stark.

And if the inflation price in your foremost bills go up greater than your wage (e.g. medical inflation tends to outpace core inflation), then it’ll be even worse.

Add within the impending GST hike of two%, and also you’ll quickly see that maintaining your cash within the financial institution might most likely not be the wisest factor to do.

How can I cease my financial savings from being eroded by inflation?

There are 2 methods to beat inflation: both in the reduction of in your bills, or develop your cash. However should you’re already working on a lean funds and have nowhere else to chop, you’ll should develop your cash as an alternative. This may be finished by way of a wide range of devices – fastened deposits, endowment funds, and even investments.

On the time of writing, the best fastened deposit is:

- Hong Leong Finance: 0.90% p.a. for 36 months (minimal $20,000)

- CIMB: 0.75% p.a. for 18 months (minimal $10,000)

With charges like these, it’s no marvel that savers at the moment are turning to short-term endowment plans with 1, 2 or 3 years of dedication. Not solely does it hold their funds protected (e.g. from scammers), but additionally permits them to at the least get extra again than what they might have in any other case had they left it within the financial institution.

In the event you’re in search of charges greater than 1%, listed below are another devices you’ll be able to take into account as properly:

- Singapore Financial savings Bond (SSB): 0.71% p.a. for the primary 12 months (minimal $500) or a median return of 1.41% p.a. in 3 years

- GREAT SP Collection 6: 1.68% p.a. after 3 years (minimal $10,000)

In the event you choose an choice that retains full liquidity in trade for a decrease payout price, then the SSB may very well be a sensible choice – you get 0.71% within the first 12 months, and should you depart it to compound, this grows to 1.17% after 2 years, and 1.41% on the finish of three years.

Nonetheless, should you already know now that you just’re unlikely to want the cash for the following 3 years, then you is perhaps higher off making use of for the GREAT SP Collection 6 as an alternative, as you’ll get a better price of 1.68% p.a. after 3 years. What’s extra, you’ll be able to choose to receives a commission the 1.68% every year, so that you get some money whereas ready throughout these 3 years. In any other case, you may as well depart the payout to build up so that you just stroll away with a doubtlessly greater payout upon maturity of the coverage.

However what if banks increase their rates of interest anytime quickly?

With the Fed’s rate of interest hike final week (with extra to come back later this 12 months), some individuals are cautious and are hoping that this may in flip, result in our banks right here in Singapore to begin providing greater rates of interest on financial savings accounts as properly. But even the Fed has said so themselves that they may or may not be able to roll out their hikes because of the uncertain environment, so it’s as much as readers in the event that they need to depend on this occurring.

My view is, even when that occurs, banks will probably implement conditions for shoppers to fulfil earlier than they get to benefit from the greater curiosity. This might embody standards akin to having to spend extra in your bank card, add usually to your deposits each month, take up a house mortgage with the financial institution, and even buy one in every of their investments or insurance coverage merchandise earlier than you qualify. In spite of everything, this has turn out to be the brand new norm for high-yield financial savings accounts in Singapore the place shoppers are made to “work” to get a better curiosity.

Besides that should you can’t meet their standards or have already maxed out this avenue (the upper rates of interest are often capped to a restrict e.g. the primary $80,000), then the remainder of your money continues to be successfully incomes solely the baseline rate of interest of 0.05% p.a.

Which suggests you continue to want to search out one other place on your funds.

GREAT SP Collection 6

The demand for the earlier GREAT SP Collection have been so excessive that they have been totally subscribed inside weeks of launch. Therefore, Nice Jap has not too long ago introduced that they’ve launched one other tranche – excellent news for individuals who missed out beforehand.

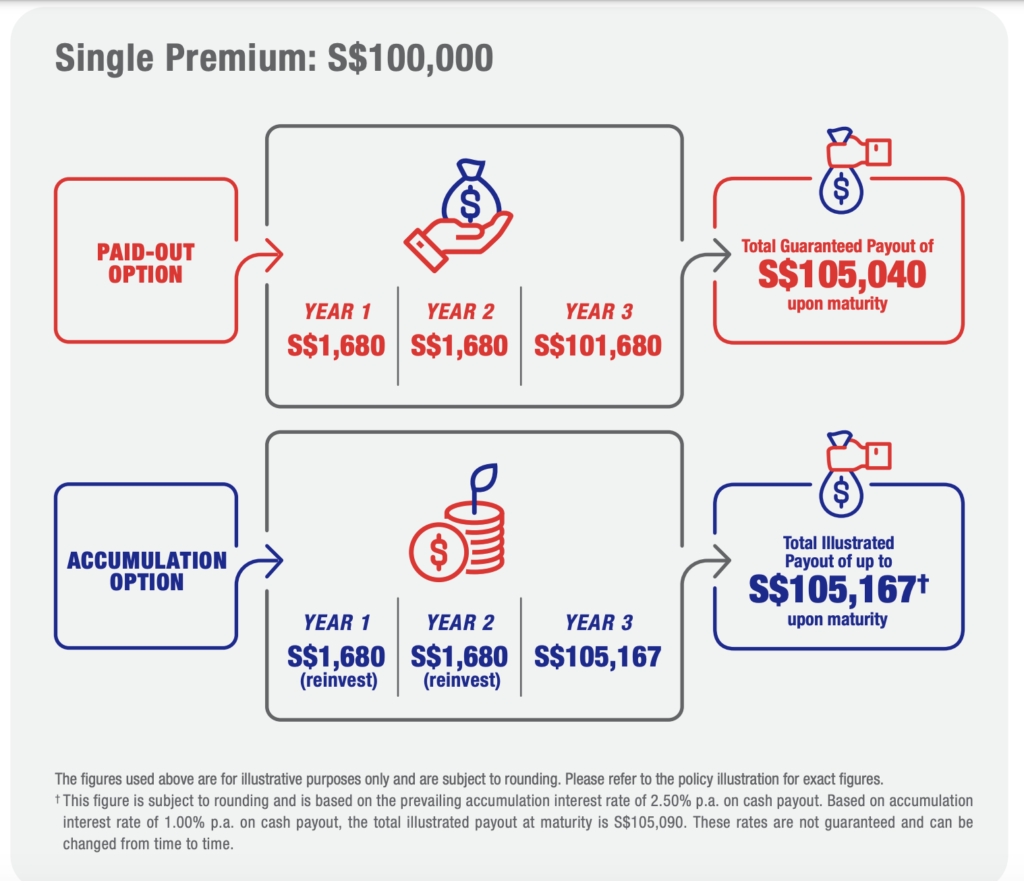

GREAT SP Collection 6 is a single-premium endowment plan and lasts for 3 years, which gives 1.68% p.a. assured returns upon maturity. Right here’s what you have to be aware of:

- 1.68% p.a. assured returns upon maturity

- Minimal premium ranging from $10,000

- Assured returns is utilized to complete premium quantity (not like a tiered payout mannequin) i.e. you could possibly join with $100,000 and nonetheless get 1.68% p.a. on the complete sum upon maturity

- Comes with insurance coverage protection in opposition to loss of life and complete and everlasting incapacity (TPD)

- No medical examination or underwriting required

Who it may very well be good for

So long as you may have spare money that isn’t incomes something greater than at the least 1.5% for the following 3 years, then it’s price trying out GREAT SP Collection 6.

Apparently, lots of my readers subscribed to the earlier tranches on behalf of their aged mother and father, because it was:

- a great way to not solely defend their funds (because the capital is assured upon maturity)

- a good price of return

- and in addition get the advantages of primary insurance coverage protection whereas doing so

It’s also vital to think about your choices in opposition to different options i.e. the place else can you place this sum of cash, and would possibly you have the ability to safe a better price of return there? Lots of my readers’ have aged mother and father who’re now not incomes an revenue / don’t use a bank card / now not have a house mortgage to finance. Normally, these individuals wouldn’t have the ability to meet the same old standards set by sure financial institution accounts and thus don’t qualify for greater curiosity.

After all, observe that placing your cash in a financial institution / fastened deposits offers you the flexibleness to withdraw anytime with none penalty in your authentic capital, not like short-term endowment plans.

If short-term endowment plans sound like one thing you’ll discover advantageous (whether or not you may have $10k, $20k, $50k, $200k or extra), you can check out more information on GREAT SP Series 6 here.

Disclosure: This put up is written in collaboration with Nice Jap, who fact-checked the offered product details about GREAT SP Collection 6. All opinions on this put up are mine.

T&Cs apply. Protected as much as specified limits by SDIC.

This commercial has not been reviewed by the Financial Authority of Singapore.

The data introduced is for normal data solely and doesn’t have regard to the precise funding aims, monetary scenario or specific wants of any specific individual. You could want to search recommendation from a monetary adviser earlier than making a dedication to buy this product. In the event you select to not search recommendation from a monetary adviser, you must take into account whether or not this product is appropriate for you.

Essential Word: As shopping for a life insurance coverage coverage is a long-term dedication, an early termination of the coverage often includes excessive prices and the give up worth (if any, that’s payable to you) could also be zero or lower than the full premiums paid.

[ad_2]

Source link

")

{kind=link}