[ad_1]

Company tax revenues boomed in 2021 and a few supporters of the 2017 Tax Cuts and Jobs Act argue that the large tax reductions within the invoice deserve the credit score (Wall Street Journal, Goodspeed and Hassett). However there’s a significantly better rationalization: Final 12 months’s sturdy financial development, excessive inflation, and pandemic-related reduction laws elevated each company earnings and the taxes enterprise paid.

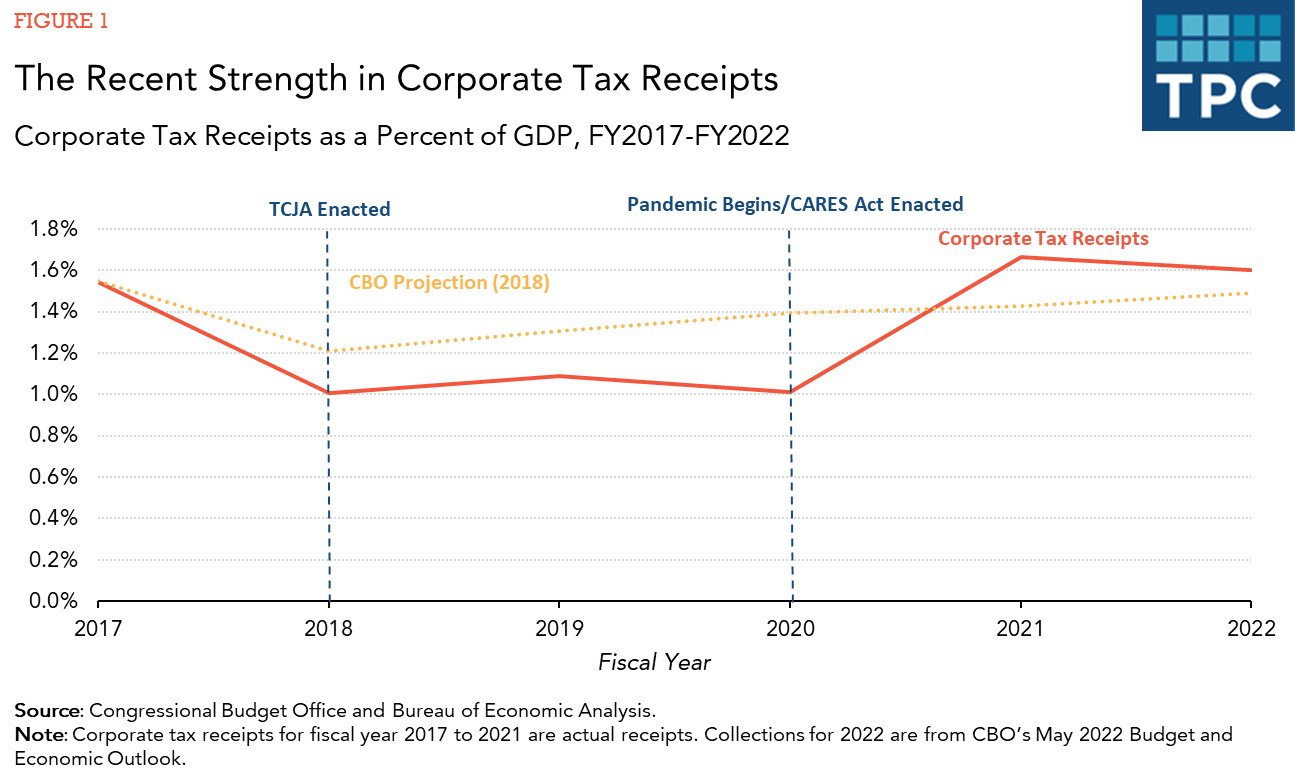

Quickly after the TCJA was handed, the Congressional Finances Workplace (CBO) forecast company tax receipts would fall from 1.5 p.c of Gross Home Product (GDP) in 2017 to 1.2 p.c in 2018 and 1.3 p.c in 2019 and stay under the 2017 share till 2022 (Determine 1). Precise company tax receipts fell even farther to 1.0 p.c of GDP in 2018 and 1.1 p.c in 2019. The onset of the pandemic in early 2020 drove the financial system into recession and stored company tax receipts low.

In 2021, company tax receipts grew dramatically to 1.7 p.c of GDP, increased than CBO’s 2018 forecast. For 2022, CBO now forecasts company tax receipts will stay sturdy however fall to 1.6 p.c of GDP, solely barely increased than it predicted in 2018.

The explanations are fairly clear: In 2021, the financial system grew at its quickest tempo in three many years and inflation rose at its highest charge in 4 many years. From early 2020 to early 2021, Congress handed a number of payments designed each to cushion the financial and public well being impression of the pandemic and assist the financial system recuperate.

These measures will pump greater than $5 trillion into the financial system over their respective 10-year funds horizons in comparison with the TCJA that totaled $1.9 trillion. The Fed’s accommodative financial coverage additionally stimulated the financial system.

Fiscal stimulus and simple cash raised the demand for items and companies a lot sooner than they elevated output, which was restricted by pandemic-related provide constraints. Collectively, these components drove costs increased. Basically, increased demand interprets into increased earnings for firms and better compensation for employees. Income enhance regardless of the upper compensation largely as a result of costs of products have a tendency to reply extra rapidly to elevated demand than wages.

Larger company earnings translate into increased company taxes. Income rose to a mean of 12.2 p.c of GDP in 2021, greater than a proportion level increased than the 11.1 p.c common between 2017 and 2019 (Determine 2).

Tax laws additionally performed a job in elevating company tax receipts in 2021. However a lot of that was attributable to timing modifications in reporting earnings. For instance, the TCJA accelerated deductions for enterprise investments, which lowered taxes early however elevated them later. The 2020 CARES Act permitted enterprise to make use of that 12 months’s losses to cut back prior 12 months taxes. Because of this, some companies accelerated deductions to 2020 and delayed earnings from 2020 till 2021—all meant to create or enhance 2020 losses. As well as, companies had an incentive to speed up earnings into 2021 and delay deductions till after 2021 to avoid proposed tax increases below the Construct Again Higher Act.

Some have instructed that the upper earnings have been the results of sturdy enterprise funding. Nonetheless, that is inconsistent with the information on charge of return for firms. As earnings rose from 2020 to 2021, the speed of return on property for nonfinancial companies elevated from 7.8 p.c to 9.4 p.c, increased than the typical of 8.4 p.c over 2017 and 2019. If increased funding boosted US company property throughout that interval, the pre-tax charge of return on company property would have fallen—not enhance because it did.

When Congress handed the TCJA on the finish of 2017, official scorekeepers anticipated company tax receipts would decline over the next decade. Nonetheless, after collapsing throughout the pandemic, they elevated considerably in 2021. A legislation as complete as TCJA is certain to impression the financial system and federal authorities funds, however TCJA isn’t a believable rationalization for the big current enhance in company tax receipts. As an alternative, simply look to the financial restoration, increased costs from provide and demand imbalances, the aftermath of pandemic reduction laws, and financial lodging.

[ad_2]

Source link

{kind=link}