AfterPay, Apple Pay Later, Sezzle, Zip, Klarna, Affirm, Paypal’s Pay in 4…the checklist of firms promoting 4 straightforward, no-interest funds continues to develop. However how does Afterpay work? And will these affords be too good to be true?

It actually provides one other layer of temptation to these late night time periods of scrolling and purchasing (and is definitely accepted in-store in some instances now). My middle-of-the-day, works-hard-for-her-money self is aware of we don’t want (and may’t afford) a $600 hairdryer, however my middle-of-the-night, treat-yourself self looks like 4 straightforward funds of $150 is definitely very cheap. An funding in trying good, if you’ll. Neglect the very actual proven fact that I don’t even like doing my hair…this might change every thing.

And that’s why the psychology of cash can get difficult. Finances and feelings are an influence couple liable to toxicity and our slippery brains are extra artistic than widespread core math relating to justifying purchases.

So, let’s dive into the world of prospects (each good and unhealthy) relating to straightforward pay affords, earlier than we find yourself with a purchase now, pay later yard military of wacky inflatable tube males. (Do you know you will get a set of eight for $270 or 4 straightforward funds of $67.50? What a deal!)

How Does Afterpay Work?

Afterpay, Klarna, Affirm, Sezzle, Zip, Paypal’s Pay in 4, and Apple Pay Later are all Purchase Now Pay Later (BNPL) platforms, which is a more moderen type of shopper credit score that’s rising in reputation.

Though the phrases and situations differ between lenders, BNPL companies break a purchase order whole into smaller equal installments due on a bi-weekly or month-to-month foundation. They often promote no upfront credit score checks (or a tender credit score pull, which received’t have an effect on credit score scores) and most don’t cost curiosity.

It’s rather a lot like an old-fashioned layaway plan, besides you get the merchandise with the primary cost as a substitute of the final.

How Does Afterpay Make Cash?

So, how do Purchase Now Pay Later companies like Afterpay generate income? Properly, they’re not lending out free cash to largely unvetted consumers out of the kindness of their coronary heart. (Though I’m positive they actually do need you to have that $600 hairdryer or these wacky inflatable tube males.)

Though there are late charges for missed funds, BNPL suppliers make nearly all of their cash by way of charges from the retailers, who pay between 4 and 9.5% to make use of these cost platforms.

And why would retailers pay that, when bank cards like Visa and Mastercard normally cost between 2 and 4%? As a result of 4 straightforward, no-interest funds of $67.50 will at all times be simpler to justify than one cost of $270, which leads to buyers being prepared to spend greater than they usually would at checkout.

What If the Funds Are Not-So-Straightforward?

There was a hamburger-loving character named Wimpy within the previous Popeye cartoons who would say, “I’ll gladly pay you Tuesday for a hamburger at this time,” however Wimpy didn’t have the cash for a hamburger at this time and wouldn’t on Tuesday both. Straightforward cost plan choices like Afterpay would have had Wimpy in a mountain of hamburger debt—after which what?

The true downside with BNPL platforms is that they do really feel really easy. A $100 merchandise? What’s $25 a month, particularly if the funds are interest-free? But when it turns into a behavior, it might flip into loads of completely different $25 funds per thirty days. BNPL cost choices allow you to purchase issues that you just don’t have the cash for and your sneaky “I would like that now” mind goes to have the utmost confidence within the safety of your monetary future and in your skill to remain organized and disciplined about these purchases and due dates.

Credit Karma printed a survey of 1,044 customers that exposed that 44% of respondents had used a BNPL cost technique, and of these customers 34% fell behind on making a number of funds. 72% of those that made late funds consider their credit score rating decreased because of this.

Though nearly all of BNPL companies don’t report accounts to credit score bureaus, a scenario which may change sooner or later, most BNPL companies will ship accounts in default to 3rd celebration assortment businesses, which might negatively impression your credit score rating—and result in persistent debt assortment makes an attempt that may make you remorse these 4 “straightforward” funds.

However I Nonetheless Wish to Purchase the Factor

Fortunately, we now have a risk-free resolution for wanting one thing you possibly can’t afford proper now. We name it BeforePay:

(Some individuals name it saving or budgeting, however let’s face it, that lacks pizzazz.)

You’ll be able to nonetheless make straightforward no-interest funds however on no matter cost schedule you need. Right here’s how one can activate an identical function in your YNAB funds:

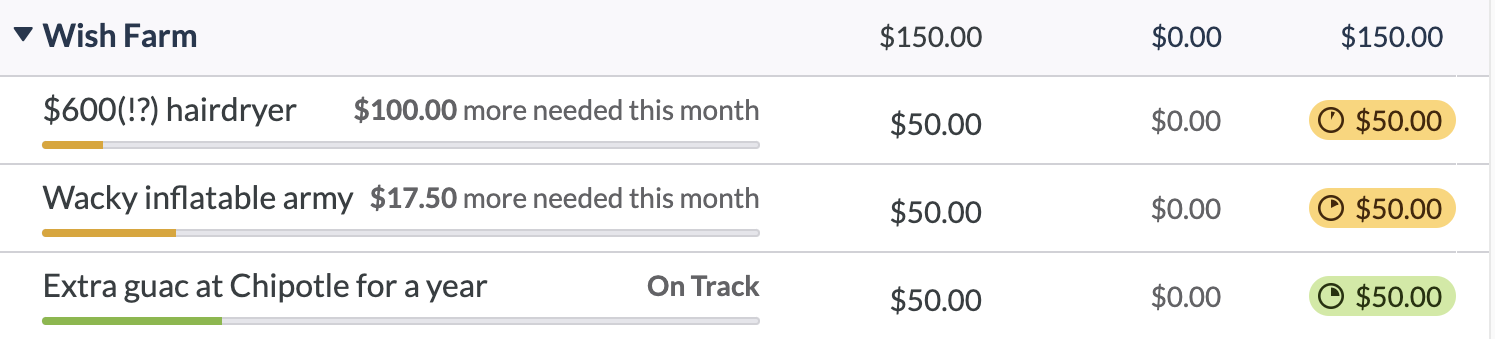

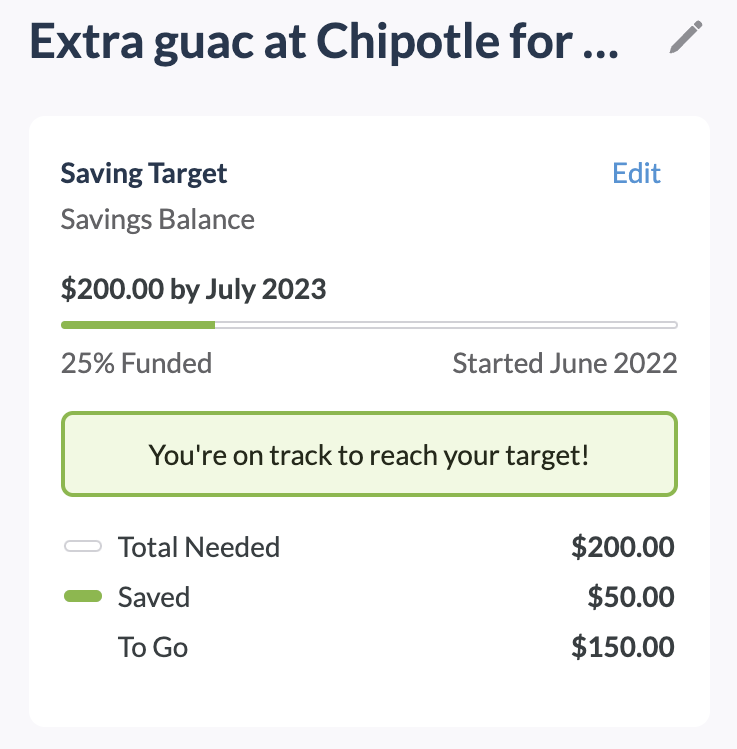

Step 1: Create a wish farm.

Step 2: Set a savings target and assign cash to that class.

Step 3: Purchase no matter you need as soon as your goal is totally funded. One and accomplished at time of buy. Free and clear.

(I don’t have an image of this half as a result of my targets usually are not totally funded. And since I’ll speak myself out of that hairdryer earlier than then anyway.)

With Apple leaping into the Purchase Now Pay Later sport, and plans in place for BNPL platforms to issue actual cards that work like a debit card (however not!), installment plans are going to proceed to develop in reputation.

Proceed with warning. Purchase what you possibly can afford. Whereas tempting, delaying funds is a method of stealing out of your future. Make a funds, plan the place you need your cash to go, and benefit from the freedom that comes with fewer funds.

Inquisitive about budgeting and wish to see the way it works? Strive a free 34-day trial and see how organizing your private funds can change your life.

{kind=link}