[ad_1]

A assessment of FWD Essential Sickness Plus insurance coverage

Once I was in my early 20s, I met an insurance coverage agent who instructed me that essential sickness insurance coverage was a good-to-have, reasonably than essential.

“You see ah, should you get most cancers, most individuals should be hospitalised. Right? Then on this case, are you able to declare the invoice out of your hospitalisation plan? Sure. So, you have to be getting the perfect and highest hospitalisation protection as a substitute, reasonably than getting lesser protection as a result of you want to reserve price range for essential sickness insurance coverage as properly. Somemore essential sickness insurance coverage is so costly!”

Whereas I’m paraphrasing her phrases as a result of it has been over a decade since that dialog, her reasoning the truth is influenced me for the subsequent few years into considering that essential sickness insurance coverage was pointless. In order that was precisely what I did – I acquired the very best protection for Built-in Protect Plan (IP) and none for essential sickness (CI).

It wasn’t till later after a couple of issues occurred that I began to alter my thoughts:

These incidents confirmed me that essential sickness insurance coverage is a must have. Not just for myself, but additionally my household as properly.

And whenever you’re battling CI, it may be a long-term battle that stops you from working, leading to a heavy toll in your funds and emotional well being. By skipping CI insurance coverage, it means you have to to spend your individual financial savings to pay for medical therapies in addition to day by day requirements. The state of affairs turns into much more dire when you’ve got dependent(s) to look after, as their bills will nonetheless should be paid one way or the other.

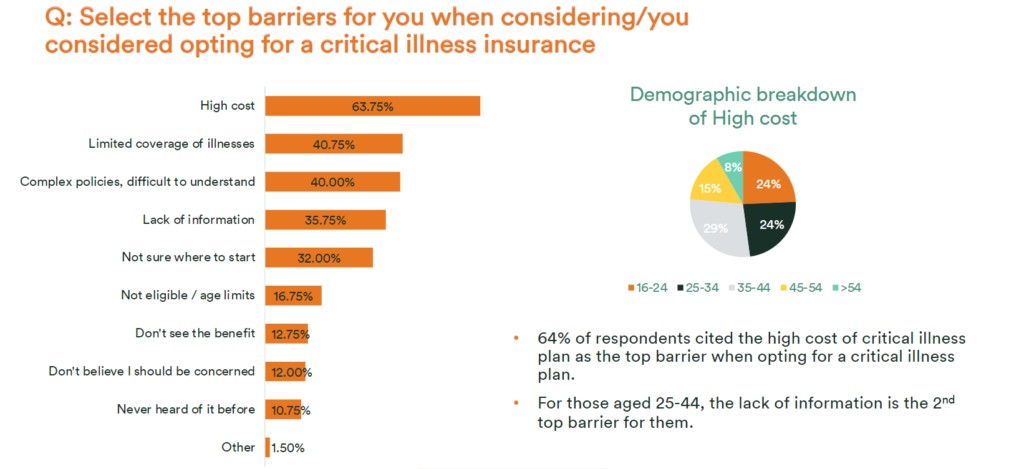

Sadly, many in Singapore proceed to go away this hole unaddressed. The highest causes embody the excessive value and restricted protection, which suggests shoppers aren’t at all times getting worth for his or her buck even when they pay for CI safety.

To get lined for all the 37 critical illnesses outlined in the framework by the Life Insurance Association of Singapore (LIA) usually equates to paying a better and dearer premium – one which not everybody could have the price range for.

What if I merely need monetary safety for the extra widespread essential sicknesses in Singapore?

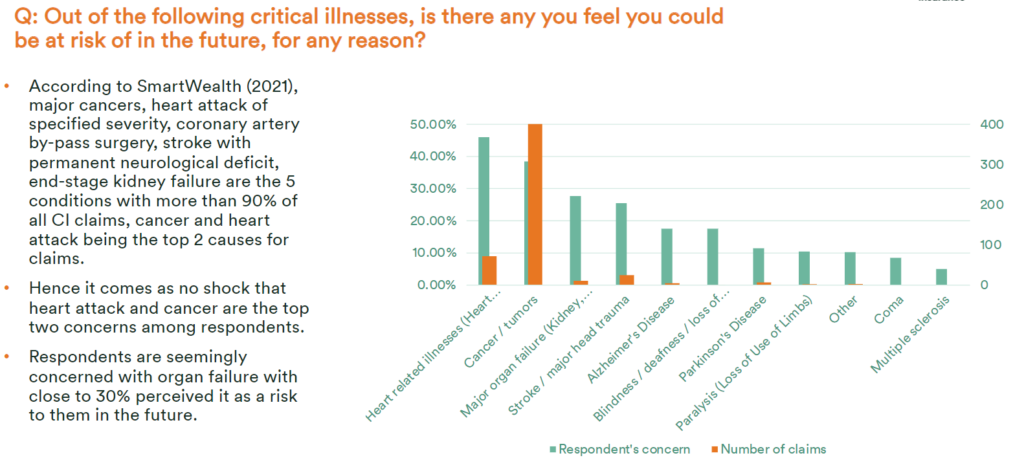

Based on Gen Re’s “2012 Dread Illness Survey” revealed in 2015, 90% of essential sickness claims in Singapore are attributable to most cancers, stroke and coronary heart assaults.

On this case, you may go for a standalone plan like FWD’s Big 3 insurance instead, which gives you financial protection against these 3 most commonly claimed critical illnesses with a much lower price compared to a regular CI plan.

That may permit you to nonetheless get lined even should you’re on a leaner price range.

However what if I’ve made a declare and get recognized with one other CI at a later age?

Sadly, the draw back of many standalone CI plans out there is that they solely provide a single payout (i.e., when you’ve made a declare in your coverage for a CI situation, the coverage terminates, and you might be now not protected).

It then turns into extraordinarily tough (or virtually unimaginable) to buy one other coverage that may cowl you, must you develop one other CI later, years down the street. Virtually no insurer will settle for your case, and even when any does, you’ll possible be topic to premiums loading and/or a number of exclusions.

Given our longer life expectancy, extra superior diagnostics (permitting us to establish circumstances earlier) and higher medical therapy (extra folks get well reasonably than move on from the situation), it’s due to this fact not shocking that many insurers have since launched CI plans with a number of payouts lately.

However after all, in change for the longer and extra complete protection, these CI plans with a number of payouts could include a better premium value.

How do multi-pay CI plans work?

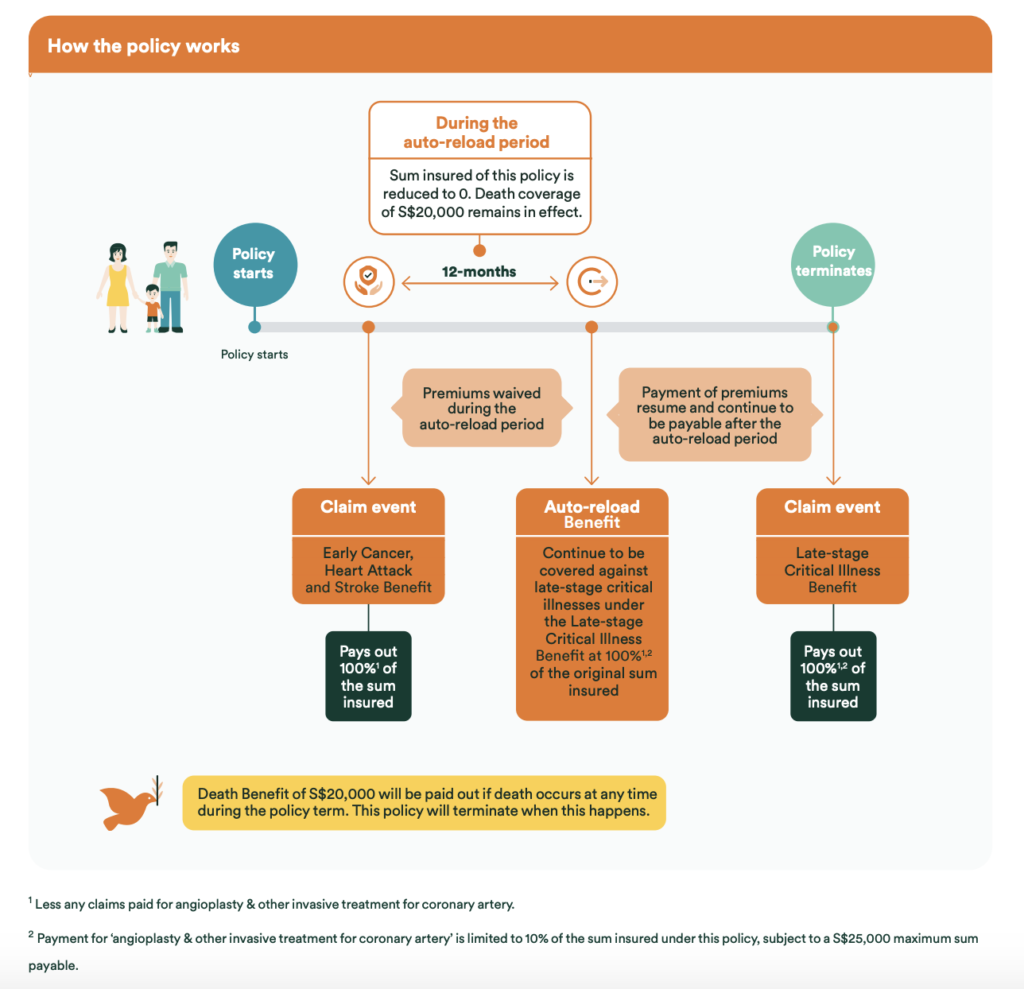

Most CI plans with a number of payouts in Singapore lets you make a number of claims within the unlucky occasion that you simply get recognized with a late-stage essential sickness after an early-stage essential sickness declare.

Relying on the insurer, these usually embody a ready or reset interval of anyplace from 12 months to three years in between claims.

Price sensible, there’s a risk that you could have to pay at the very least $1,500* every year, or larger.

*For a 30-year feminine non-smoker for $100k cowl on an area insurer’s multi-pay CI plan.

One potential concern when you find yourself contemplating a CI plan with a number of payouts could possibly be the upper premium value as in comparison with standalone plans. Nevertheless, there are digital insurers that provide such plans and infrequently priced at extra reasonably priced ranges.

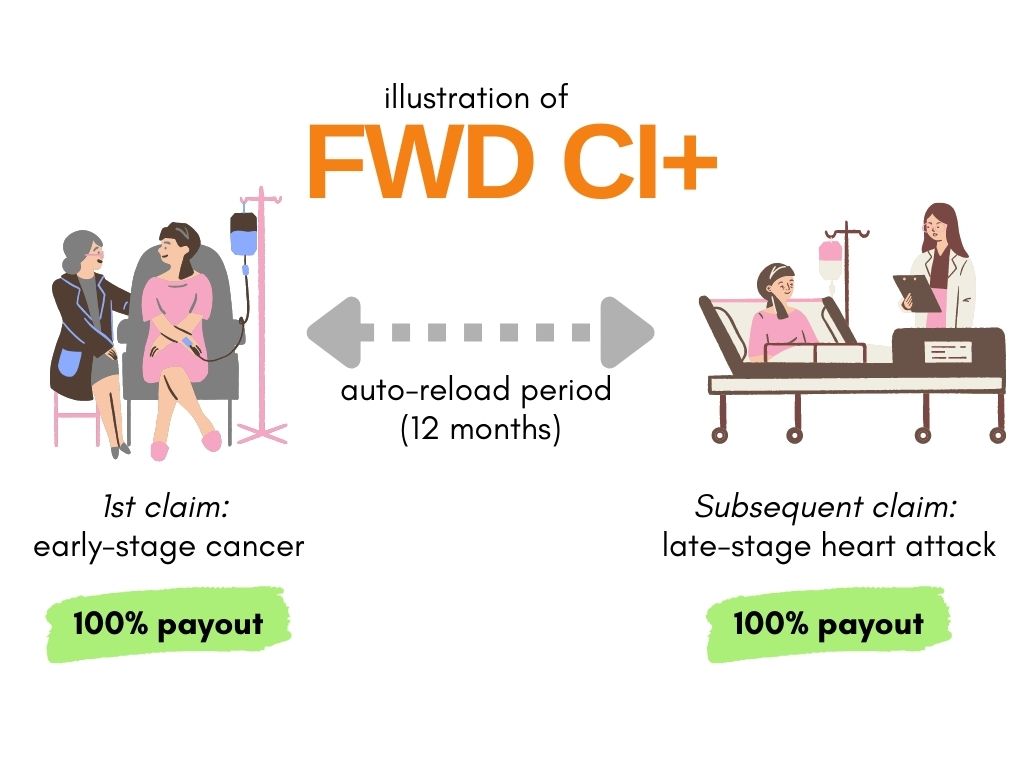

Therefore, one answer could possibly be to discover insurance policies by shopping for insurance coverage straight on-line, since they’re usually priced at extra reasonably priced ranges. For these of you who desire a coverage that continues to guard you for late-stage essential sicknesses even after you’ve claimed for early-stage most cancers, coronary heart assault or stroke, you may think about FWD’s newest Essential Sickness Plus insurance coverage. It will probably cowl you for late-stage essential sicknesses even after an early-stage most cancers, coronary heart assault or stroke declare. You’ve got the pliability to cowl your self up till age 85 and the coverage will solely terminate after a payout of 100% of the coverage’s sum insured for a late-stage CI or when the Dying Profit has been paid.

What can I anticipate from FWD Essential Sickness Plus insurance coverage?

The primary protection that you simply get from the plan are:

- Early-stage protection for most cancers, coronary heart assault and stroke

- Late-stage protection for 37 essential circumstances together with Alzheimer, extreme dementia and benign mind tumour

- Dying good thing about S$20,000

Relying in your declare state of affairs, you may get a number of payouts, as much as 200% of your sum insured.

By way of prices, they’re comparatively reasonably priced – a 30-year-old feminine non-smoker will simply must pay S$69.90 monthly to be lined till she’s 65 years previous.

| For time period cowl until the age of 65 | Sum insured | ||

| Buyer Profile | S$100k | S$200k | S$300k |

| Feminine, age 30, non-smoker | S$69.9/month | S$139.79/month | S$209.7/month |

| Male, age 35, non-smoker | S$76.13/month | S$152.25/month | S$228.37/month |

| Feminine, age 40, non-smoker | S$124.45/month | S$248.89/month | S$373.34/month |

| Male, age 45, non-smoker | S$148.39/month | S$296.78/month | S$445.17/month |

Premiums on FWD Essential Sickness Plus insurance coverage are additionally levelled all through your coverage time period, making it simpler so that you can plan your price range within the coming years. A professional tip is to get your protection earlier as insurers are likely to cost you decrease premium whenever you buy the plan at a youthful age.

There’s additionally an optionally available ICU Profit that gives you with as much as one other 100% payout within the occasion that you’re hospitalised in an intensive care unit for five steady days on invasive life help, be it for an unexpected accident and even an unknown illness sooner or later.

How a lot protection do I have to get?

Referencing Seedly’s figures on cancer treatment costs here, the estimates are at S$8,000 to S$17,000 every month for most cancers therapy. For late-stage most cancers, therapy prices can simply add as much as S$100k to $200k every year.

Whereas larger protection is at all times higher, your choice ought to in the end be based mostly on how a lot you may afford to pay for.

With FWD Essential Sickness Plus insurance coverage, you will have the pliability to lower your protection in your sum insured at a later stage (e.g. when your kids have grown up and are now not financially depending on you) in multiples of S$50k. Nevertheless, do be aware that you simply gained’t be capable to enhance your coverage protection after your buy, so you might wish to take into consideration what’s the highest vs. the bottom protection that you simply want, after which work backwards from there.

TLDR of FWD Essential Sickness Plus insurance coverage

If you happen to’ve been considering of getting a CI plan with a number of payouts however have been placing it off due to the excessive prices, then you definitely’ll like FWD Essential Sickness Plus insurance coverage as a first-of-its-kind safety plan that covers you for early-stage CI claims (most cancers, coronary heart assault and stroke) in Singapore and full monetary safety for late-stage CIs.

Whereas the early-stage protection is probably not as complete (vs different plans that cowl all 37 circumstances) at first look, coronary heart assault, stroke and most cancers make up 90% of all essential sickness claims, and this plan lets you strike a great steadiness between affordability and complete protection. If that’s what you care most about, then this could possibly be the proper plan for you.

Sponsored Message In terms of your well being, be sure to have 100% of what you want, whenever you want it. FWD Essential Sickness Plus insurance coverage offers you complete essential sickness protection which you can purchase on-line, with no medical check-up required. Get lined for early-stage most cancers, coronary heart assault and stroke whereas nonetheless being lined sooner or later for any of the 37 late-stage essential sicknesses. Better of all, it's 100% lump sum payout, so you may select to make use of the cash nevertheless it finest helps you. Phrases and circumstances apply. From now till fifth August 2022, get 30% off your first-year premium whenever you use promo code “SGBBCI30”. Get a quote here today.

Disclosure: This publish is written in collaboration with FWD. All opinions are that of my very own. As my life circumstances differ from yours, you need to search recommendation from a licensed consultant for customised recommendation in your monetary wants. The knowledge together with any comparability is supposed purely for informational functions and shouldn't be relied upon as monetary recommendation. This presentation accommodates solely common data and doesn't have any regard to the particular funding aims, monetary state of affairs and the actual wants of any particular particular person. All insurance coverage purposes are topic to FWD's underwriting and acceptance. This doesn't represent a proposal to purchase or promote an insurance coverage services or products. Please check with the precise phrases and circumstances, particular particulars and exclusions relevant within the coverage paperwork that may be obtained from our authorised product distributor. You might want to search recommendation from a monetary adviser consultant for a monetary evaluation earlier than buying a coverage appropriate to fulfill your wants. Shopping for medical insurance merchandise that aren't appropriate for you might influence your potential to finance your future healthcare wants. This coverage is protected beneath the Coverage Homeowners’ Safety Scheme which is run by the Singapore Deposit Insurance coverage Company (SDIC). Protection in your coverage is automated and no additional motion is required from you. For extra data on the sorts of advantages which can be lined beneath the scheme in addition to the bounds of protection, the place relevant, please contact us or go to the GIA/LIA or SDIC web-sites (www.gia.org.sg or www.lia.org.sg or www.sdic.org.sg). This commercial has not been reviewed by the Financial Authority of Singapore. Info is correct as at 27 July 2022.

[ad_2]

Source link

")

%20(1).png "How to Manage Money With Irregular Income")

{kind=link}