Mortgage fee forecast for subsequent week (Dec. 27-31)

Mortgage charges proceed to fluctuate. As of December 23, they had been again down to three.05% on common.

The current dip adopted 4 weeks the place mortgage charges had been flat or rising.

This again–and–forth displays outbreaks of the Omicron Covid–19 variant weighing down shopper sentiment paired with constructive financial restoration.

Trying ahead, charges appear more likely to rise once more until additional shutdowns are required to fight Omicron.

Find your lowest mortgage rate. Start here (Dec 24th, 2021)

On this article (Skip to…)

>Associated: 7 Tips to get the lowest refinance rate

Will mortgage charges go down in January?

Mortgage charges decreased barely on the finish of December. However they need to flip round in January and maintain climbing all through 2022.

Latest declines could be pinned on the Omicron variant. The extremely–contagious pressure has precipitated renewed worry about touring, eating out, in–individual procuring, and different key financial actions that had been simply starting to normalize earlier than the variant hit. This precipitated a minor slowdown in the pace of economic growth and pushed mortgage charges barely decrease.

However consumers’ outlook on the economy remains to be constructive total. And the forces driving rates of interest upward – together with document–excessive inflation – are nonetheless current.

Maybe most significantly, the Federal Reserve lately introduced it will pace up the tempo of tapering to fight these excessive inflation numbers.

The Fed expects to finish its mortgage stimulus program by March or April of 2022. That would imply considerably larger mortgage charges within the first quarter of the yr.

Keep in mind that the Fed’s bond purchases all through the pandemic had been holding mortgage charges artificially low. Because the Fed pulls again (‘tapers’) these purchases, mortgage charges will nearly actually rise.

As of its final assembly, the Fed expects to finish its mortgage stimulus program by March or April of 2022. That could mean significantly higher mortgage rates within the first quarter of the yr.

For now, although, rates of interest are nonetheless at historic lows.

In the event you’ve postpone refinancing a house or buying a brand new house, January 2022 could possibly be the time to do it. The window to make the most of at this time’s low–fee surroundings might shut rapidly.

Get started shopping for mortgage rates (Dec 24th, 2021)

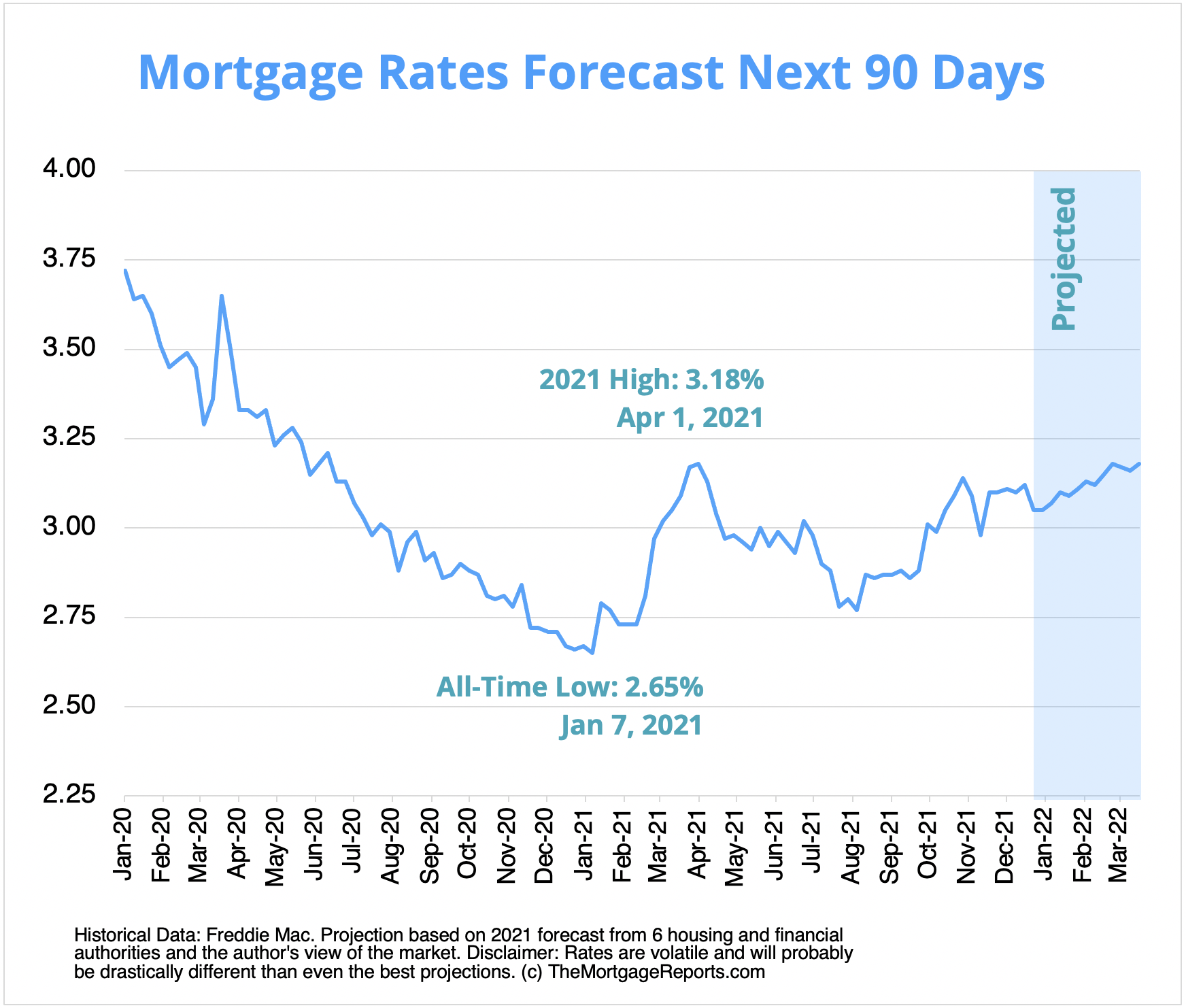

Mortgage rates of interest forecast subsequent 90 days

Regardless of some minor financial slowdown as a result of Omicron variant, shopper sentiment remains to be sturdy. Supplied the financial system continues to develop and shed its Covid worries, mortgage charges ought to rise slowly within the first quarter of 2021. As all the time, there is likely to be brief durations of stagnant or falling charges throughout the total upward development.

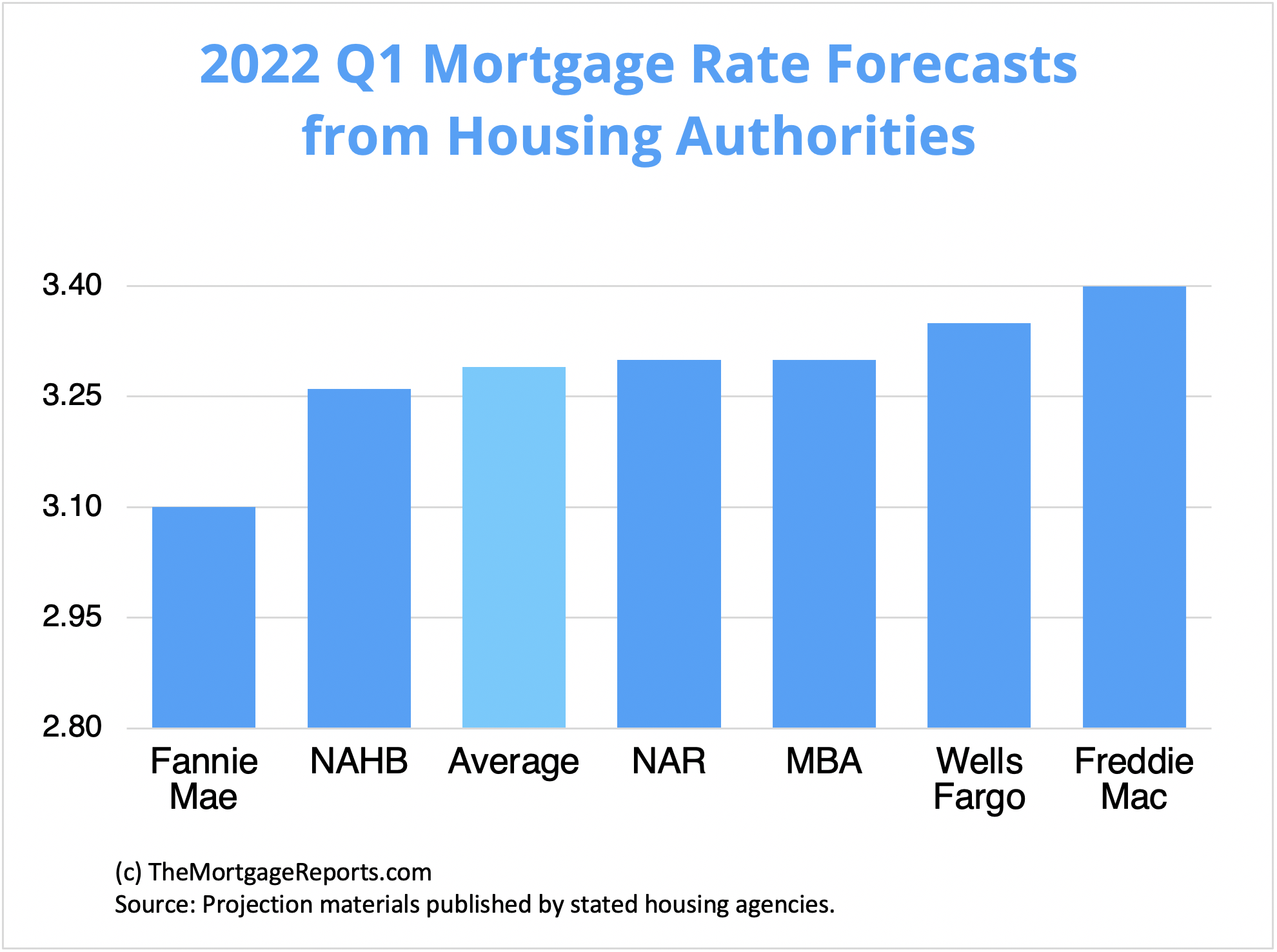

Mortgage fee predictions for 2022

Main housing authorities predict larger mortgage rates of interest within the first quarter of 2022.

Fannie Mae gives the bottom prediction, placing 30–yr mounted rates of interest at 3.10% by the tip of Q1. Wells Fargo and Freddie Mac are on the different finish of the spectrum, predicting 30–yr charges as excessive as 3.35% or 3.40% in early 2022.

| Housing Authority | 30-Yr Mortgage Fee Forecast (Q1 2022) |

| Fannie Mae | 3.10% |

| Nationwide Assoc. of House Builders | 3.26% |

| Nationwide Affiliation of Realtors | 3.30% |

| Mortgage Bankers Affiliation | 3.30% |

| Wells Fargo | 3.35% |

| Freddie Mac | 3.40% |

| Common Prediction | 3.29% |

Present mortgage rate of interest developments

Common mortgage charges took a step down final week (Dec. 23). The typical 30–yr mounted fee went from 3.12% to three.05%, based on Freddie Mac’s weekly fee survey.

Per the survey, 15–yr mounted charges fell from 2.34% to 2.30%, whereas the typical fee for a 5/1 ARM fell from 2.45% to 2.37%.

| Month | Common 30-Yr Fastened Fee |

| January 2021 | 2.74% |

| February 2021 | 2.81% |

| March 2021 | 3.08% |

| April 2021 | 3.06% |

| Could 2021 | 2.96% |

| June 2021 | 2.98% |

| July 2021 | 2.87% |

| August 2021 | 2.84% |

| September 2021 | 2.90% |

| October 2021 | 3.07% |

| November 2021 | 3.07% |

Supply: Freddie Mac

Mortgage charges are transferring away from the document–low territory seen in 2020 and 2021.

However remember that charges are nonetheless extremely–low from a historic perspective.

Simply three years in the past, in December 2018, 30–yr charges had been at 4.75% based on Freddie Mac’s survey. And in December 2019 they had been averaging round 3.75%.

So if you happen to haven’t locked a fee but, don’t lose an excessive amount of sleep over it. There are nonetheless nice offers available – particularly for debtors with sturdy credit score.

Simply be sure you store round to search out the most effective lender and lowest fee to your distinctive scenario.

Mortgage fee developments by mortgage sort

Many mortgage consumers don’t understand there are various kinds of charges in at this time’s mortgage market.

However this information will help house consumers and refinancing households discover the most effective worth for his or her scenario.

Following are 3–month mortgage fee developments for the preferred varieties of house loans: typical, FHA, VA, and jumbo.

| November 2021 | October 2021 | September 2021 | |

| Conforming Mortgage Charges | 3.27% | 3.27% | 3.20% |

| FHA Mortgage Charges | 3.38% | 3.39% | 3.25% |

| VA Mortgage Charges | 2.96% | 2.96% | 2.81% |

| Jumbo Mortgage Charges | 3.24% | 3.19% | 3.17% |

Supply: Black Knight Originations Market Monitor Report

Which mortgage mortgage is greatest?

One of the best mortgage for you is dependent upon your monetary scenario and your targets.

As an illustration, if you wish to purchase a excessive–priced house and you’ve got nice credit score, a jumbo mortgage is your greatest wager. Jumbo mortgages permit mortgage quantities above conforming mortgage limits – which max out at $ in most elements of the U.S.

Alternatively, if you happen to’re a veteran or service member, a VA mortgage is sort of all the time the suitable selection.

VA loans are backed by the U.S. Division of Veterans Affairs. They supply extremely–low charges and by no means cost personal mortgage insurance coverage (PMI). However you want an eligible service historical past to qualify.

Conforming loans and FHA loans (these backed by the Federal Housing Administration) are nice low–down–payment options.

Conforming loans permit as little as 3% down with FICO scores beginning at 620.

FHA loans are much more lenient about credit score; house consumers can typically qualify with a rating of 580 or larger, and a much less–than–good credit score historical past may not disqualify you.

Lastly, take into account a USDA mortgage if you wish to purchase or refinance actual property in a rural space. USDA loans have beneath–market charges – just like VA – and lowered mortgage insurance coverage prices. The catch? It’s essential stay in a ‘rural’ space and have average or low earnings to be USDA–eligible.

Find your lowest mortgage rate (Dec 24th, 2021)

Mortgage fee methods for January 2022

Mortgage charges are on the rise, and that development ought to proceed in January 2022 and past. However there are nonetheless nice alternatives available for house consumers and refinancing owners.

Listed here are only a few methods to remember if you happen to’re mortgage procuring within the subsequent few months.

Make lenders compete to your fee

Greater charges typically aren’t nice information for debtors. However there could also be a silver lining.

When charges rise, fewer owners are motivated to refinance. Which means lenders are seeing slower enterprise and will likely be extra keen to usher in new prospects.

You need to use this surroundings to your benefit by making mortgage lenders compete for your refinance loan.

By getting only a few quotes and asking lenders to match or beat the competitors, you may decrease your rate of interest, refi closing prices, or each.

Buying round can simply prevent 1000’s of {dollars} over the lifetime of your mortgage. And making lenders compete will maximize your financial savings. So don’t be afraid to ask for a greater deal.

Save extra by procuring round

Mortgage lenders are nonetheless providing traditionally low charges to good debtors. However there’s a catch.

You’ll be able to’t simply search for the bottom fee marketed on-line. As a result of the charges lenders promote aren’t out there to everybody.

These gives sometimes symbolize debtors with good credit score, 20% down or extra, and a sterling credit score historical past.

These standards received’t apply to everybody. The speed you’re truly provided is dependent upon:

- Your credit score rating and credit score historical past

- Your private funds

- Your down cost (if shopping for a house)

- Your property fairness (if refinancing)

- Your mortgage–to–worth ratio (LTV)

- Your debt–to–earnings ratio (DTI)

To determine what fee a lender can give you primarily based on these elements, you must fill out a mortgage software. Lenders will examine your credit score and confirm your earnings and money owed, then offer you a ‘actual’ fee quote primarily based in your monetary scenario.

You need to get 3–5 of those quotes at minimal. Then examine them to search out the most effective supply.

Search for the bottom fee, but in addition take note of your annual proportion fee (APR), estimated closing prices, and ‘low cost factors’ – additional charges charged upfront to decrease your fee.

This would possibly sound like a whole lot of work. However you may shop for mortgage rates in under a day if you happen to put your thoughts to it. And shaving only a few foundation factors off your fee can prevent 1000’s.

Compare mortgage and refinance rates. Start here (Dec 24th, 2021)

Mortgage rate of interest FAQ

Present mortgage charges are averaging 3.05% for a 30–yr mounted–fee mortgage, 2.30% for a 15–yr mounted–fee mortgage, and a pair of.37% for a 5/1 adjustable–fee mortgage, based on Freddie Mac’s newest weekly fee survey. Your particular person fee could possibly be larger or decrease than the typical relying in your credit score rating, down cost, and the lender you select to work with, amongst different elements.

Mortgage charges might lower subsequent week (December 27–31, 2021) relying on the severity of Omicron variant case numbers. If the curve retains trending upward, it might result in charges falling regardless of inflation development and the Fed altering its insurance policies.

It’s unlikely mortgage charges will go down in 2022. Inflation has been climbing at a document fee over the previous couple of months. And the Fed is planning to wind down its mortgage stimulus and lift rates of interest prior to initially anticipated. Each these elements ought to result in considerably larger mortgage charges in 2022.

Sure, it’s very possible mortgage charges will improve in 2022. Hight inflation, a powerful housing market, and coverage modifications by the Federal Reserve ought to all push charges larger in 2022. The one factor more likely to push charges down can be a significant resurgence in critical Covid instances and additional financial shutdowns. However, whereas it might assist mortgage charges, nobody is hoping for that consequence.

Freddie Mac remains to be citing common 30–yr charges within the low–3 p.c vary. However do not forget that charges range loads by borrower. These with good credit score and huge down funds might get beneath–common rates of interest, whereas poor–credit score debtors and people with non–QM loans would possibly see rates of interest nearer to 4 p.c. You’ll have to get pre–accepted for a mortgage to know your actual fee.

For probably the most half, trade consultants don’t count on the housing market to crash in 2022. Sure, house costs are over–inflated. However most of the threat elements that led to the 2008 crash are usually not current in at this time’s market. Low stock and large purchaser demand ought to maintain the market propped up subsequent yr. Plus, mortgage lending practices are a lot safer than they was. Which means there’s not a sub–prime mortgage disaster ready within the wings.

On the time of this writing, the bottom 30–yr mortgage fee ever was 2.65 p.c. That’s based on Freddie Mac’s Major Mortgage Market Survey, probably the most broadly–used benchmark for present mortgage rates of interest.

Locking your fee is a private determination. You need to do what’s proper to your scenario quite than attempting to time the market. In the event you’re shopping for a house, the suitable time to lock a fee is after you’ve secured a purchase order settlement and shopped to your greatest mortgage deal. In the event you’re refinancing, it’s best to be sure you examine gives from not less than 3 to five lenders earlier than locking a fee. That stated, charges are rising. So the earlier you may lock in at this time’s market, the higher.

That is dependent upon your scenario. It’s a great time to refinance in case your present mortgage fee is above market charges and you may decrease your month-to-month mortgage cost. It may additionally be good to refinance if you happen to can change from an adjustable–fee mortgage to a low mounted–fee mortgage; refinance to eliminate FHA mortgage insurance coverage; or change to a brief–time period 10– or 15–yr mortgage to repay your mortgage early.

It’s typically price refinancing for 1 proportion level, as this will yield vital financial savings in your mortgage funds and complete curiosity funds. Simply ensure that your refinance financial savings justify your closing prices. You need to use a mortgage calculator or communicate with a mortgage officer to crunch the numbers.

Begin by selecting a listing of three–5 mortgage lenders that you simply’re fascinated about. Search for lenders with low marketed charges, nice customer support scores, and suggestions from associates, household, or an actual property agent. Then get pre–accepted by these lenders to see what charges and costs they’ll give you. Evaluate your gives (Mortgage Estimates) to search out the most effective total deal for the mortgage sort you need.

What are at this time’s mortgage charges?

Low mortgage charges are nonetheless out there. Join with a mortgage lender to search out out precisely what fee you qualify for.

Show me today’s rates (Dec 24th, 2021)

1As we speak’s mortgage charges are primarily based on a every day survey of choose lending companions of The Mortgage Reviews. Rates of interest proven right here assume a credit score rating of 740. See our full loan assumptions here.

Chosen sources:

- https://www.blackknightinc.com/class/press–releases

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/analysis/datasets/refinance–stats/index.web page

The data contained on The Mortgage Reviews web site is for informational functions solely and isn’t an commercial for merchandise provided by Full Beaker. The views and opinions expressed herein are these of the creator and don’t mirror the coverage or place of Full Beaker, its officers, guardian, or associates.

{kind=link}