Yesterday John Warren posted a thought experiment on the weblog. Following an introduction that’s price studying however which I can’t repeat right here he said:

Right here is the thought experiment, and the query. It is vitally easy. What would occur if the Authorities determined to print £1Trn of crisp new notes in all of the denominations; however – crucially – didn’t flow into it: simply positioned it within the (empty and handy) vaults in Threadneedle Road; the fiat equal of Gold. How would that seem within the accounts of presidency and BofE, and what occurs to the recording of the Nationwide Debt. How does the stability sheet look now? We may differ the phrases; print a single £1Trn bank-note, then we all know it is going to by no means flow into (that variant was put to me by a younger economist – who has damaged free from the standard knowledge).

My speedy thought is that this can be a variant on the trillion-dollar coin suggestion from Krugman and others within the USA. I feel the variant is admittedly essential, together with on this case. There are two causes for that.

First, technically £1 trillion of banknotes not issued don’t signify debt: they’re merely a pay as you go value of the manufacture of tokens of debt that could be issued. As such the double entry is credit score manufacturing value within the earnings account, debit inventory and work in progress on the Financial institution of England stability sheet, with that debt retaining worth till the be aware design ceases for use, when this inventory will develop into nugatory. I counsel that the printing has no consequence in any respect till issued just because there isn’t any legal responsibility on the stability sheet. And that’s essential: what it says is that the Financial institution of England is, like all financial institution, unable to create cash with out third-party involvement [see footnote].

Nevertheless, the Treasury can and does creates cash with worth when minted by way of its subsidiary the Royal Mint and I feel it may be efficiently argued that they don’t seem to be within the official cash provide figures, though acknowledged by the Financial institution of England as base foreign money. It is because coin (and there are solely £4.2 billion price in existence) will not be accounted for as liabilities while in distinction notes most positively are within the nationwide debt, if solely through the Financial institution of England internet contribution to that debt. I ought to add that I’ve tried to get straight solutions on each these points from HM Treasury, the BoE, and ONS, with none success from any of them. However, the proof from the accounting is I feel unambiguously what I’ve instructed.

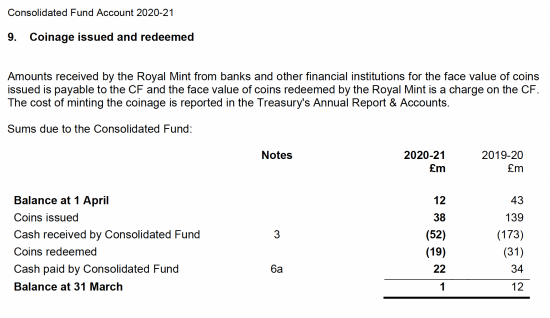

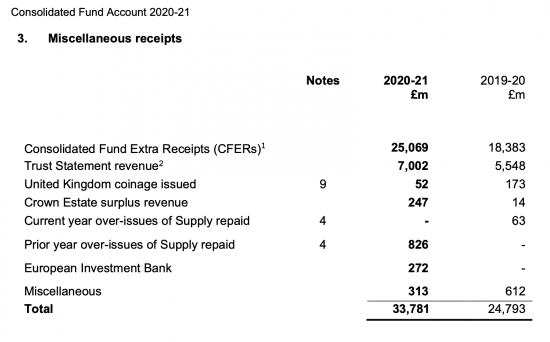

I ought to, having mentioned so, clarify that how the Treasury accounts for the excess / loss on coin creation is unclear in its accounts, largely as a result of after routine manufacturing prices for the present cash in subject the web sum could be very small, however the accounting for his or her subject can, for these prepared to pursue the purpose, be found in the Consolidated Fund Accounts. That is from them for 2021:

The important level right here is that the worth of the cash issued have been earnings within the Consolidated Fund:

There’s due to this fact a debt with the Financial institution of England – the Consolidated fund stability elevated.

However the place, after prices of subject, does the revenue within the Treasury go? A credit score within the earnings assertion has to have a stability sheet consequence in any case. There isn’t a indication I can discover of that: the web sum might be too small to require disclosure, in equity (and to confuse issues the price of creating the cash is confusingly within the Treasury’s accounts). And but that is the age-old seignorage – the revenue that goes to the coin creator from turning metallic into coin, and it does exist. It will most positively exist if a £1 trillion coin was created.

As famous above, the worth of that coin could be recorded as earnings within the Consolidated Fund – which is a belief account of the Treasury, and so a part of authorities funding. Base cash would enhance by £1 trillion in consequence. However the place does that £1 trillion credit score within the earnings assertion of the consolidated fund stream to on the stability sheet? It may’t go to liabilities as a result of there may be already a credit score within the earnings assertion, so the one place it will probably go is to the Reserves of HM Treasury. And in the meantime, the Financial institution of England would merely document it as a banking transaction.

So what does a rise in reserves imply? It’s, in impact, a rise in capital, which is, after all, precisely what occurs right here. The federal government did create capital for the banking system to make use of. The ensuing accounting for such a coin displays actuality, which the accounting for QE and central financial institution reserve accounting doesn’t.

The extra attention-grabbing level is that so far as I can see this acquire doesn’t fall out on consolidation of the accounts. When that takes place there’s a debit left from the Financial institution of England accounts, which is to base cash, and a credit score to authorities reserves. I’ll fortunately be proven to be unsuitable. However within the time I’ve had out there that seems to be the accounting results of this.

What’s the consequence? My suggestion is that it’s fairly simple. That debit to base cash can be utilized. How? To switch the central financial institution reserve accounts held by the industrial banks with the Financial institution of England, I counsel. The coin would possibly must be damaged down into some smaller items in that case beginning with ten million-pound cash and possibly transferring as much as some billion-pound ones. However the level is, the Financial institution of England may insist that the industrial banks enter into an alternate of their central financial institution reserve accounts for cash to the extent that the Financial institution of England desired, and people cash would then be an asset on the industrial financial institution stability sheets guaranteeing their solvency, and allowing inter-bank settlement as properly by registering costs on them, however on the identical time no curiosity want be paid on them by the Financial institution of England. That final subject goes away.

And what of that credit score within the reserves of the Complete of Authorities Accounts? That’s then correctly described because the ‘nationwide capital’. That’s, it’s the worth injected by the federal government into the financial system for the general public good. However what the federal government doesn’t need to do is then pay anybody for the privilege of getting finished the precise factor for society.

Lastly, does this stop financial coverage utilizing altering rates of interest to be transmitted into the financial system through the CBRAs? It doesn’t. Keep in mind, this labored in 2008 when the balances have been round £40 billion. Close to sufficient £900 billion is just not required for this function now. Possibly £100 billion could be ample for that cause. It’s laborious to think about greater than £200 billion is required. Curiosity on all the surplus is saved. That’s fairly one thing by way of financial justice, and all for issuing some cash.

So is that this the Krugman trick? I counsel not. That was supposed to cancel debt. This doesn’t. It recognises QE cancelled gilts and redenominates the central financial institution reserve accounts, for positive, however the purpose is completely different. The purpose is to cancel curiosity funds and to recognise capital. I don’t see that because the Krugman aim, and counsel that is in any case higher because it displays what really occurs, merely repricing it.

[Footnote] That is additionally true with quantitative easing: the concept that a Financial institution of England subsidiary is the counterparty to Financial institution of England cash creation in quantitative easing is just not true. The Financial institution of England’s Asset Buy Facility is actually run by a subsidiary wholly beneath the financial management of the Treasury, which underwrites all its losses. That’s the reason it isn’t consolidated within the Financial institution of England accounts. though this isn’t admitted.

{kind=link}