You’re not a rooster; nevertheless, having a nest egg that meets your retirement wants is simply as golden.

What’s a nest egg, and the way a lot must you save for retirement?

A nest egg is a big sum of money saved in property, investments or financial institution accounts for retirement.

Should you’re fascinated by early retirement or plan on working till 65 or longer, take into account what might put a wrench in your objectives.

Sadly, not everybody with a nest egg lives to get pleasure from what they’ve labored so exhausting to construct.

At this time, I need to discover expectations throughout retirement and whether or not you’ll use your nest egg.

Planning Your Retirement Nest Egg

Do you ever end up scanning the obituaries to see if somebody that handed away?

Name her loopy, however Mrs. CBB does this, and I puzzled why she was intrigued for the longest time.

For one, she’s discovered individuals from her previous that had died or mother and father and grandparents that she’d met.

She feels that between the age of 55 and up are probably the most utilized years of retirement financial savings.

Adults of their 20s and 30s are working to make a mark on this world, and it’s robust to speculate.

With housing costs not in attain, the main focus of planning a nest egg has shifted.

Paying your self first by way of a wage, financial savings, or investments is probably going a stretch.

First, pay the lease or mortgage, together with bills, debt and financial institution loans.

Some individuals can’t get to that time with out juggling invoice funds or bank cards to make ends meet.

There isn’t any cash left to spend money on a nest egg for retirement, and good luck if there ever can be.

Dwelling on authorities pensions in the event you’ve labored lengthy sufficient in Canada covers the fundamentals.

Earlier than, Throughout And After Retirement

Maybe you’re a two-income household; the youngsters are transferring away and coming again dwelling.

The state of affairs is just not unprecedented as a result of college students and dealing younger adults can’t afford to dwell.

Dad and mom might really feel obliged to help a baby who strikes again in or require them to pay a nominal lease.

What about in case you have getting old mother and father you have to take care of?

The checklist of what might occur earlier than, throughout and after retirement is neverending.

Issues can go south rapidly if one thing is not noted, similar to a Authorized Will or monetary info.

Begin wrapping your self in crimson tape and be ready for the hustle of the residing and the lifeless.

Making Life Selections Based mostly On Expertise

Planning our retirement nest egg got here years earlier than Mrs. CBB, and I tied the knot.

We didn’t find out about retirement or investing in class; we discovered by way of life experiences.

Beginning a household for some individuals is commonly placed on maintain resulting from monetary instability and a tricky name to make.

I do know this could be a tender spot for individuals who imagine there may be by no means an appropriate time for parenthood.

In my 20s, after I purchased my second home, I made a decision that profession got here first, then a household.

Rising up within the UK, I’ve seen an abundance of households residing in poverty situations, and it scared me.

My mother and father should not rich and oversaw their {dollars} by residing a frugal life-style.

I needed to work for no matter I wished and sometimes felt that I used to be completely different from another youngsters.

Maybe that’s the place a part of me mentioned I wished to attend, and I’m glad I did.

3.5 million youngsters are rising up in poverty within the UK. It’s one of many worst charges within the industrialised world and successive governments proceed to battle to convey it into line. Struggling & and not using a voice, ‘Poor Children’ shines a lightweight on this urgent challenge.

Studying The Newspaper Finance Part

Mrs. CBB and I delivered the newspapers for years once we had been little kiddos.

We had been accountable and knew the way to return the proper cash to our prospects.

Some prospects didn’t pay their weekly invoice, in order that they had been reduce off from additional deliveries.

We discovered a useful lesson about paying payments or dealing with the implications.

You don’t pay; you don’t get—finish of the story.

We’d learn town newspaper virtually every day as there was at all times an additional for our routes.

Heaps could be mentioned a few baby studying the newspaper in a corrupt world of cash and politics.

Nonetheless, newspaper schooling allowed us to learn what was taking place and why.

We didn’t have cellphones, computer systems or entry to the web within the ’70s and ’80s.

We knew we didn’t need to go with out and opted for a greater monetary future.

You’ll be able to translate that to, we didn’t need to dwell in poverty and wished to make important adjustments.

Early Financial institution Account Guides Our Retirement Nest Egg

Though we didn’t know one another, we saved all our cash in a high-interest checking account.

My mother and father moved 20 occasions after I was two years outdated, and it prompted me many social issues.

How is a child presupposed to make buddies in the event that they always change colleges and lose buddies?

My social nervousness carried into maturity, so I had few shut buddies and typically closed up throughout a dialog.

We labored by way of highschool (UK equal) and socked cash away each probability.

Concurrently our schooling, there was a way of wanting freedom from monetary fear.

My best world was a profession first, marriage and shopping for a home that may accommodate a household.

Mrs. CBB purchased a brand new Dodge mini-van at 0% curiosity and paid it off in 5 years.

At 30 years outdated, Mrs. CBB and her accomplice purchased a house that was 3000 sq toes from high to backside.

The home was presupposed to be a nest egg funding the place her ex was set to retire.

That didn’t occur, and though she might purchase one other home, she didn’t select that route.

As a substitute, she rented a room, stored saving cash, and continued investing in a registered retirement savings plan (RRSP).

Her employer provided an employer pension the place they matched, so she took benefit and went all-in.

Upon leaving, our monetary advisor moved the pension right into a Locked-In Retirement Account (LIRA), which began at round $1200.

Presently, her LIRA is simply over $5000 after 13 years, however at the very least it’s rising.

How A lot Nest Egg Do We Want To Retire?

Returning to the obituary dialog, Mrs. CBB and I mentioned whether or not we wanted three million {dollars} to retire.

In 2021, I wrote a weblog publish about how our retirement plans have changed.

Right here we’re a 12 months later, and I wished to revisit that publish to see if our emotions are the identical or modified.

The reality is that it hasn’t, and greater than ever, we plan to stay put and renovate our house.

Within the final two years, there have been many individuals we all know who died earlier than they retired.

What this implies is that they don’t get to get pleasure from their retirement financial savings.

All of our buddies who know we’re debt-free assume we’re rich and dwell a unprecedented life.

Some individuals appear to neglect that whereas they had been out spending cash we had been saving it.

Being debt-free doesn’t imply you’re shielded from life obstacles, though it does cushion the blow.

Typically neglected is the potential of not being round to make use of a retirement nest egg.

How rich of a life does that develop into?

There’s a advantageous line between saving for a nest egg and watching it curler coaster till the day you want it.

That’s if the day ever comes.

Monetary Duty With A Nest Egg

Though we’re assured about our nest egg, we’ve set our son up so he may have no schooling debt or need to pay for all times insurance coverage.

There’s a non-registered funding account that we spend money on for him that comes with a withdrawal age.

We need to assume he can be answerable for his funds; nevertheless, we don’t know and should by no means know.

Offered nothing drastic occurs in our little household, he’ll ultimately be left with no matter now we have.

Mrs. CBB and I are nearer to 50 years outdated, which has triggered many feelings for us.

Though we don’t know once we will die, it’s protected to say that we don’t need to die with out spending cash.

Having no mortgage has been a blessing, and life has been incredible from a monetary standpoint.

We paid it off in 5 years, so we didn’t have to fret about rates of interest ever once more.

Do we need millions of dollars to retire, not counting our government pensions?

Most likely not, particularly if one or each of us turns into in poor health or has well being issues which we anticipate.

Jetting off on trip as we age, particularly with well being issues, could be expensive for journey insurance coverage.

Altering Our Wealth Mindset

Though we maintain constructing our nest egg, it might find yourself in our son’s arms someday.

We’re glorious with that, however we even have taken the route that life and funds should stability.

For instance, if you wish to go on vacation and have the money, then expertise the world.

You don’t need to put on second-hand garments; happening a date shouldn’t be riddled with guilt.

Being a finance blogger has taught me 4 important guidelines about saving a nest egg for tomorrow.

- Should you’re keen about one thing early in life, do it when you’re younger.

- Don’t sock all the pieces you’ve obtained into your retirement nest egg.

- Perceive what can occur as we age and the estimated prices concerned

- Dwell for right this moment and tomorrow with the potential of an early exit.

Once we are each gone, our son received’t care how a lot cash we’ve left him.

Each of us have skilled dropping a father or mother or passing away earlier than age 65 resulting from coronary heart situations.

The whole lot they ever dreamed of is gone, and whispers of I don’t need to die to linger in our minds.

Nest Egg Expectations Typically Turn into Goals

Your nest egg is nothing greater than a quantity left for many who survive you.

I’m certain somebody will want that they had executed one thing with you when you had been nonetheless alive.

I really feel budgeting and constructing a nest egg are simply as essential as paying off debt and experiencing life.

Please don’t wait till it’s too late to do what you need with your loved ones, buddies or each.

Examine your Plan B, get your priorities so as and discuss to your monetary advisor concerning the affect of retirement expectations vs potential well being issues.

Don’t cease securing your future by being glad with a legal Will and a fats financial savings account.

Perceive the prices of residing in a nursing dwelling or long-term care and planning your funeral.

Planning a comfy nest egg is critical, however don’t take it as far as to put life on maintain.

Dialogue: Have you ever ever thought-about what’s going to occur in the event you die, leaving all the pieces you saved for retirement with out having fun with it?

Please share your ideas or feedback beneath.

Thanks for stopping by to learn.

Mr. CBB

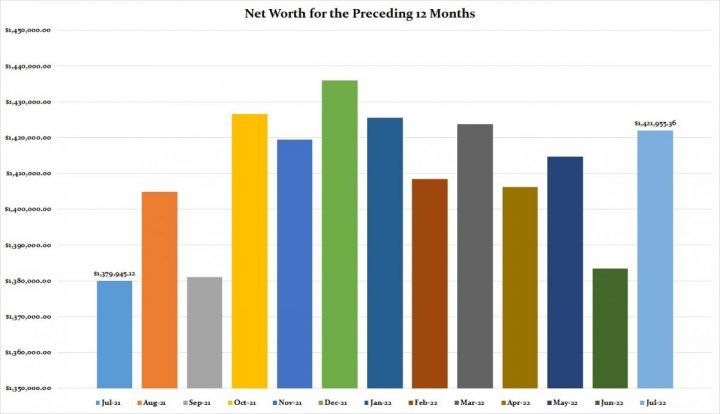

CBB Web Value For The Previous 12 Months

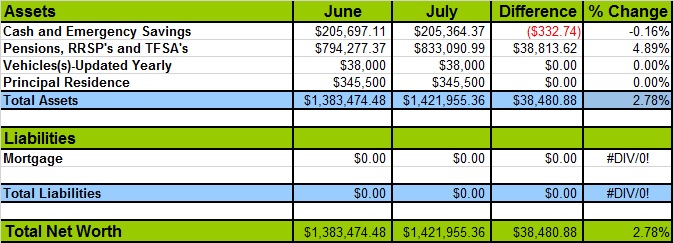

Scroll near the underside in the event you already know the way to calculate your web price to see the breakdown of our July web price.

Web Value Will increase And Decreases

The chart above displays our web price will increase and reduces all through 2021-2022.

What are your ideas about seeing your investments enhance and reduce?

Drop me your feedback beneath.

How To Calculate Your Web Value

Web price provides up your property (what you personal) after which removes your liabilities (what you owe), providing you with a web price quantity.

We like calculating our month-to-month web price to know if we’re nonetheless on monitor.

Some individuals calculate it yearly or quarterly, nevertheless it’s as much as you and the way knowledgeable you need to keep.

Web Value is solely an estimate, and never everybody makes use of the identical kind of figures to tally it up.

Figuring out Web Value

Web price = Belongings – Liabilities

Calculate your web price with our Free Cash saving Device Net worth Calculator (Canadian Budget Binder.

Web Value Losses And Positive factors 2022

Hello everybody,

Our investments, like many others, have been on a curler coaster for the previous couple of months.

It’s good to report that we did see a 2.78% enhance in July to drive up a portion of what our portfolio has misplaced.

It’s for the long-term, so now we have to maintain reminding ourselves that numbers will go up and down.

Canadian Finances Binder Web Value Updates 2022

Click on the hyperlinks beneath to learn our web price updates for 2022.

The next web price report can be in September to take a look at our August 2022 web price figures.

Subscribe To Canadian Finances Binder

I do know I’ve already mentioned it, however in the event you haven’t subscribed to Canadian Finances Binder, I’ll go away the sign-up type beneath. Mr.CBB

Subscribe To the Canadian Finances Binder And Get My Unique CBB Emergency Binder FREE!

{kind=link}