So it looks as if everybody round you has been speaking about SGS Bonds and T-bills these days. What are they, and must you comply with the gang who’ve invested their financial savings into it? Right here’s what it’s good to know earlier than you make any transfer.

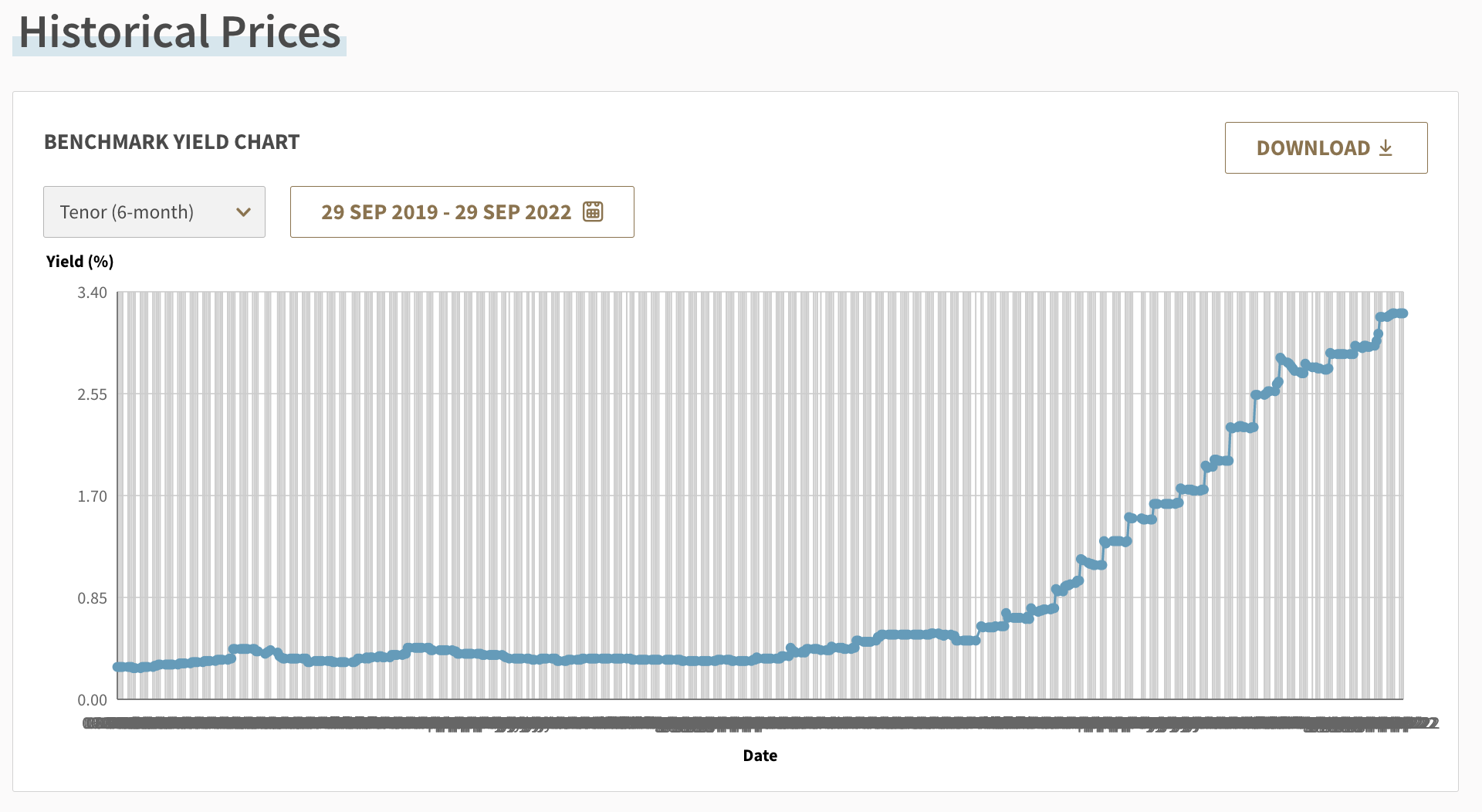

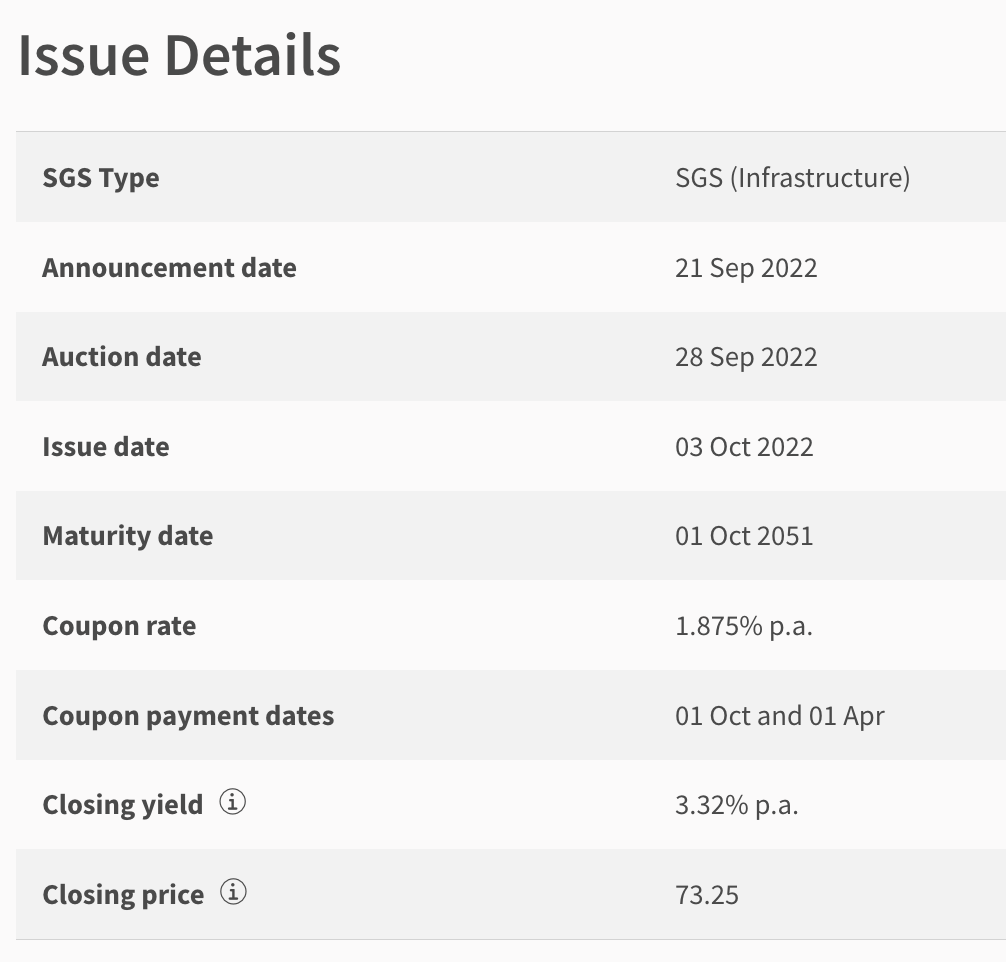

With the newest MAS T-bills cut-off yield at 3.32% p.a., Singapore’s monetary scene has been buzzing with discuss of it, even amongst non-investors and folk who’ve by no means purchased bonds earlier than.

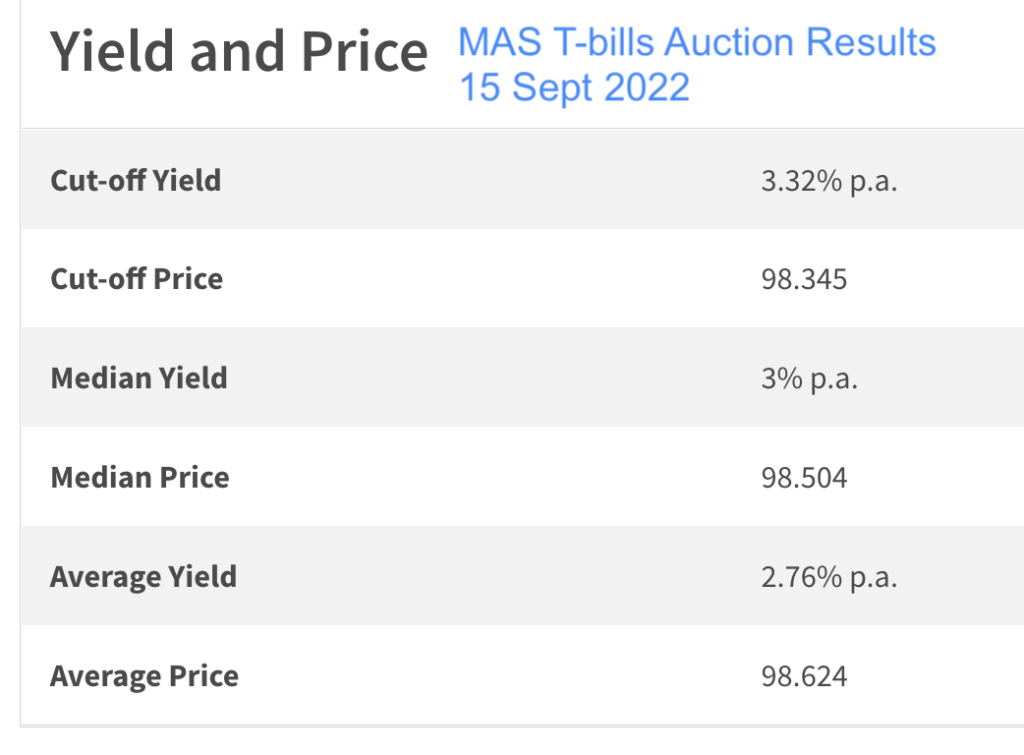

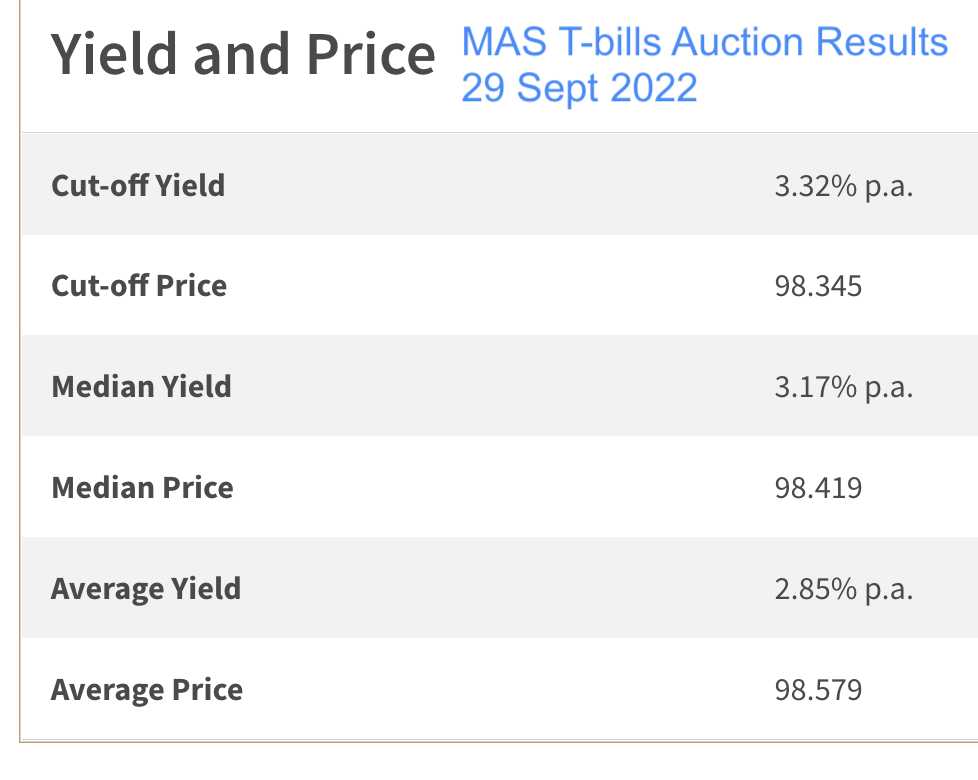

And with charges this excessive, it’s no shock that nearly everybody appears to be excited over the newest T-Payments, the place yields have gone up from 0.61% in January to three.32% p.a. for the newest auctions in September.

At these charges, even essentially the most aggressive mounted deposit appear like a weaker providing in distinction, particularly with an extended lock-up interval too. For example, the very best price now could be 2.8% p.a. supplied by RHB Financial institution for a minimal $20k placement for twenty-four months, whereas Hong Leong is providing 2.75% p.a. on a deposit of at the least $50k for a 12 months.

And as it’s, the native fixed deposits are already at their highest since the end of the Asian financial crisis almost 24 years ago.

What are Treasury Payments and Is It Price Investing In?

Singapore’s Treasury Payments (T-bills for brief) are short-term authorities securities issued at a reduction to their face worth, within the type of 6-month and 1-year T-bills. As an investor, you obtain the complete face worth at maturity, which suggests your yield may be calculated because the distinction between your bid value and the maturity value.

Simplified Explainer: If you happen to efficiently bid for and secured a 6-month T-bill on the price of three.32%, your $100k capital would now develop into $10k + $1,660 after 6 months. If you happen to managed to safe a 1-year T-bill on the identical charges, you'll have successfully “earned” $3,320. In actuality, what would have occurred is that you'd have paid $96.68 for the bond and gotten $100 upon maturity i.e. you'll have paid $96,680 and acquired $100,000 after 6 months / 1 12 months, which is the place your 3.32% yield comes from.

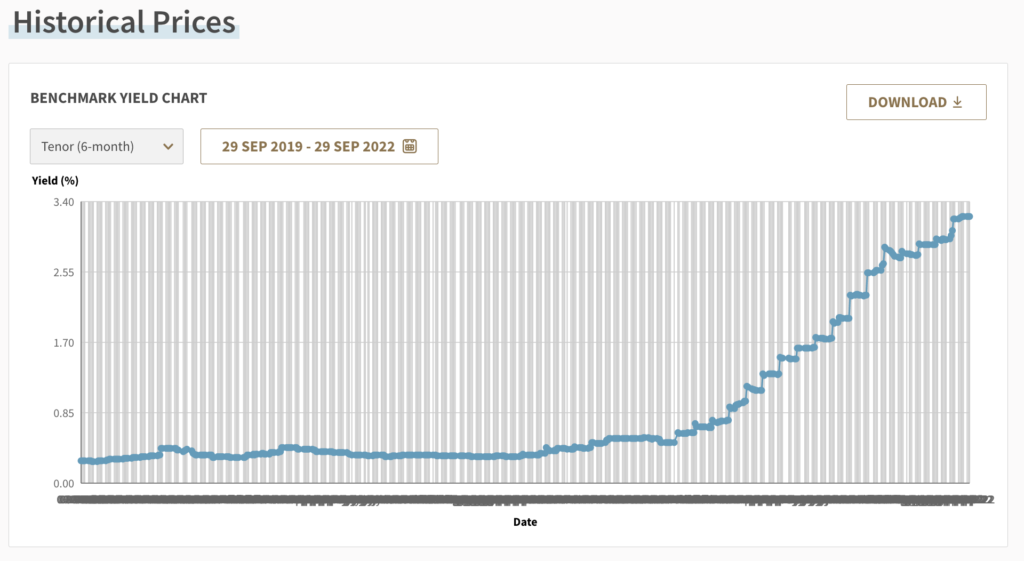

There hasn’t been a lot curiosity in T-bills previous to this 12 months and for good purpose: the yields on our native T-bills have remained pretty flat all alongside (and for the final 3 years), however began rising steeply from the beginning of this 12 months (according to the worldwide Fed’s rate of interest hikes):

My Take: If T-bill yields proceed rising and there’s no news about CPF interest rates being revised higher, I'll begin to use my CPF funds to purchase into some T-bills as soon as yields cross the prevailing CPF charges.

You may simply learn how to use for T-bills on-line, so I gained’t cowl that on this article. Nonetheless, what are the dangers that include investing in T-bills?

Dangers of Investing in T-Payments

Now, should you intend to purchase and maintain T-bills till maturity, then your danger is sort of none – since these T-bills are absolutely backed by the Singapore authorities and are to be held for less than 6-months or 1-year at most. Except you suppose the Singapore authorities goes to go bankrupt or bail on you inside this quick time-frame…a danger which I believe is sort of near zero.

Nonetheless, in case your private monetary circumstances adjustments abruptly throughout this (quick) interval and also you out of the blue want the money (earlier than maturity), you’ll then need to promote them within the secondary market.

This may be completed by going to any of the native banks and getting a quote from them.

Persevering with on the above instance, think about you've gotten $96,680 locked up in a 1-year T-bill, however you can't wait till its maturity in 2 months time to get $100,000 since you want the cash urgently now. Your financial institution quotes your $98 (as a substitute of the $100 you had been hoping for) and you are taking it, since you’re determined. You now get $98,000 as a substitute of the $100,000 you had been anticipating, taking a $1,320 “revenue” as a substitute and letting your financial institution earn $2,000 since you needed to let it go sooner than anticipated.

T-bills vs. Singapore Authorities Securities (SGS)

At any price, T-bills with their shorter maturity are a a lot better possibility than SGS bonds, which have maturities starting from 2 – 50 years.

And when you can technically promote your SGS bonds on the secondary market i.e. SGX by your self (no must undergo your financial institution), the market is extraordinarily illiquid i.e. it’s more durable to search out patrons than you suppose.

T-bills vs. Singapore Financial savings Bonds

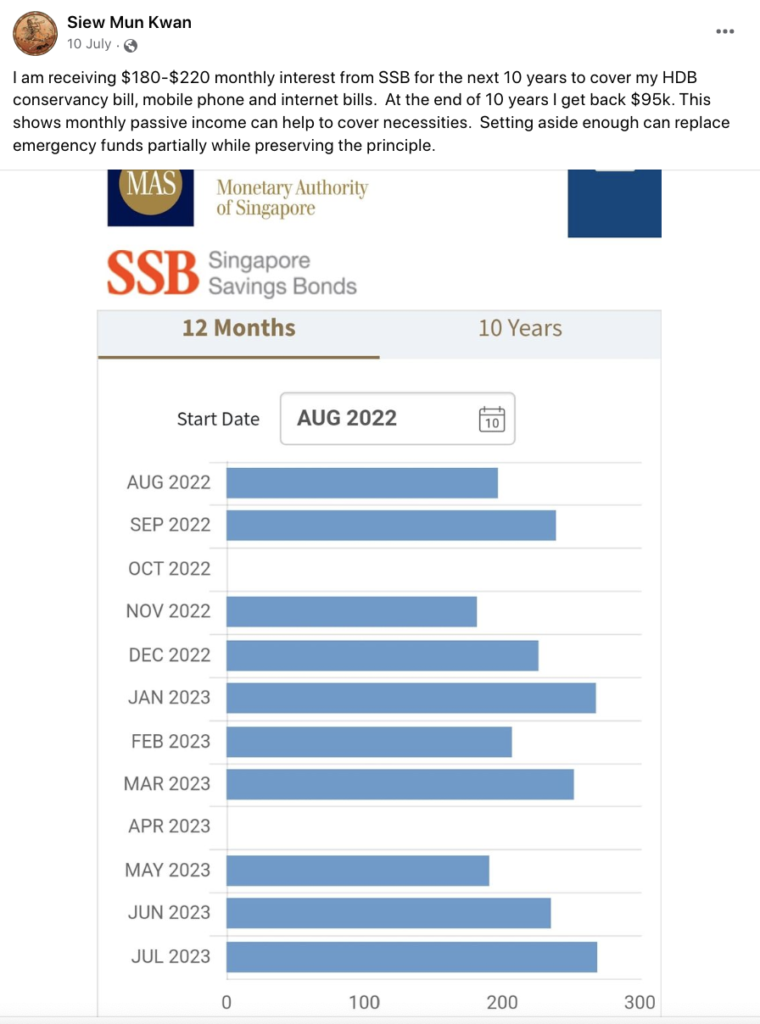

Another choice can be to contemplate Singapore Financial savings Bonds (SSBs), that are equally backed by the Singapore authorities however supply extra flexibility i.e. you may redeem your SSB items at any time.

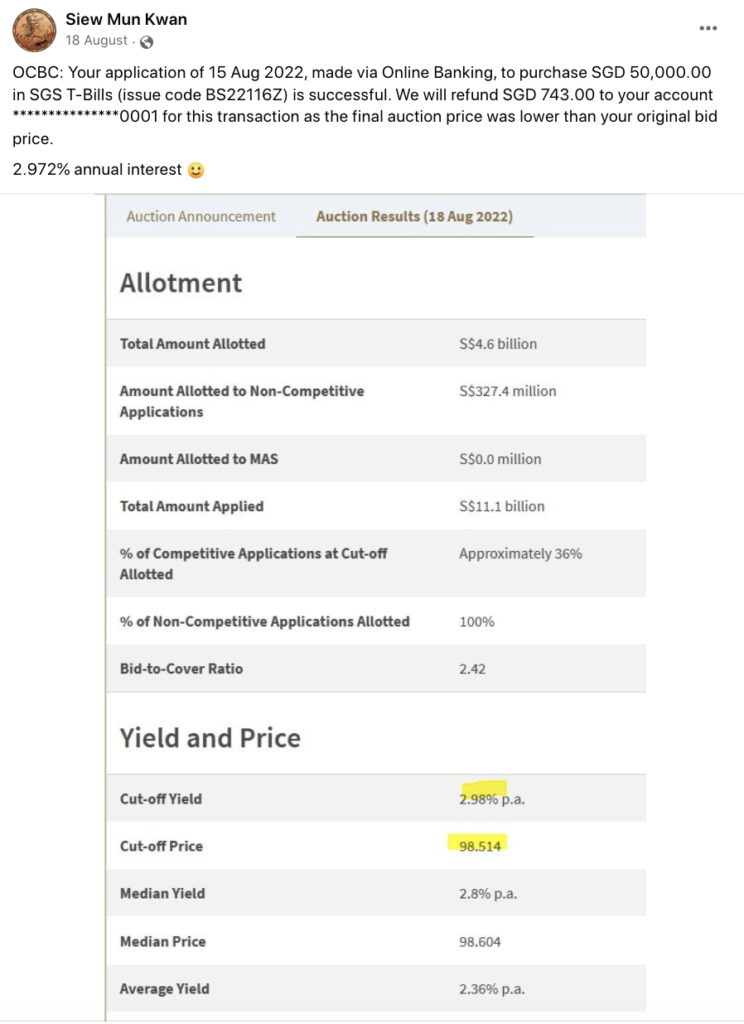

Hardworking people can strive their arms at constructing a SSB ladder i.e. replicating what this different low-risk investor, Siew Mun, has completed:

I began speaking about SSBs once they had been first launched in October 2015, however as charges had been low then (<1% for the primary 1-2 years), there was little incentive to actually construct a SSB ladder again then because it felt like an excessive amount of work for too little features.

Right now, with charges beginning at 2.6% for the primary 12 months of SSBs, low-risk buyers preferring to go for secure investments (i.e. no danger of capital loss) can think about this.

Nonetheless, even holding SSBs for 10 years (presently 2.99%) could now not be sufficient to beat inflation. Therefore, chances are you’ll need to diversify into different monetary instruments as a substitute.

Whereas T-bills are undoubtedly engaging at this cut-off date, the yields are consistently altering and it’s important to bid at every public sale i.e. there’s no assure that you’re going to get it.

If you happen to do, hooray!

And should you tried however haven’t been profitable at your prior auctions, one other funding device you may think about are money administration funds – (also referred to as Cash Market Funds (MMFs) – as a substitute.

No, they’re not backed up by the Singapore authorities, however they often supply a greater return than mounted deposits whereas supplying you with the pliability to redeem your cash anytime with no penalty.

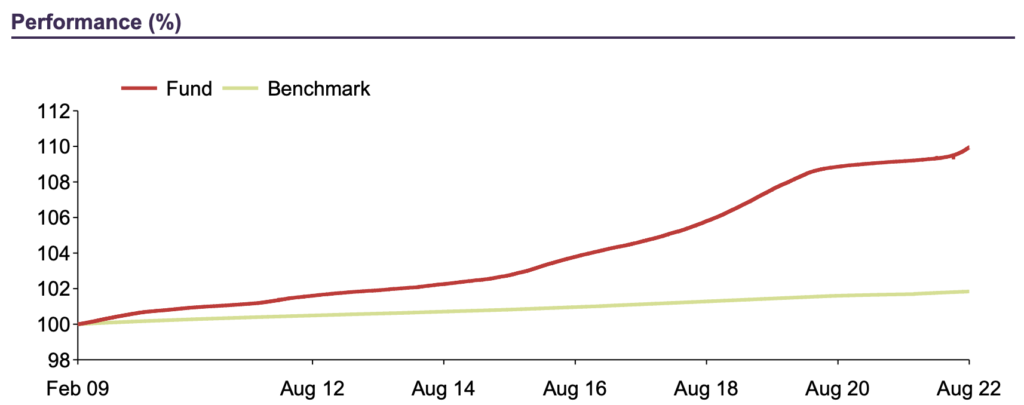

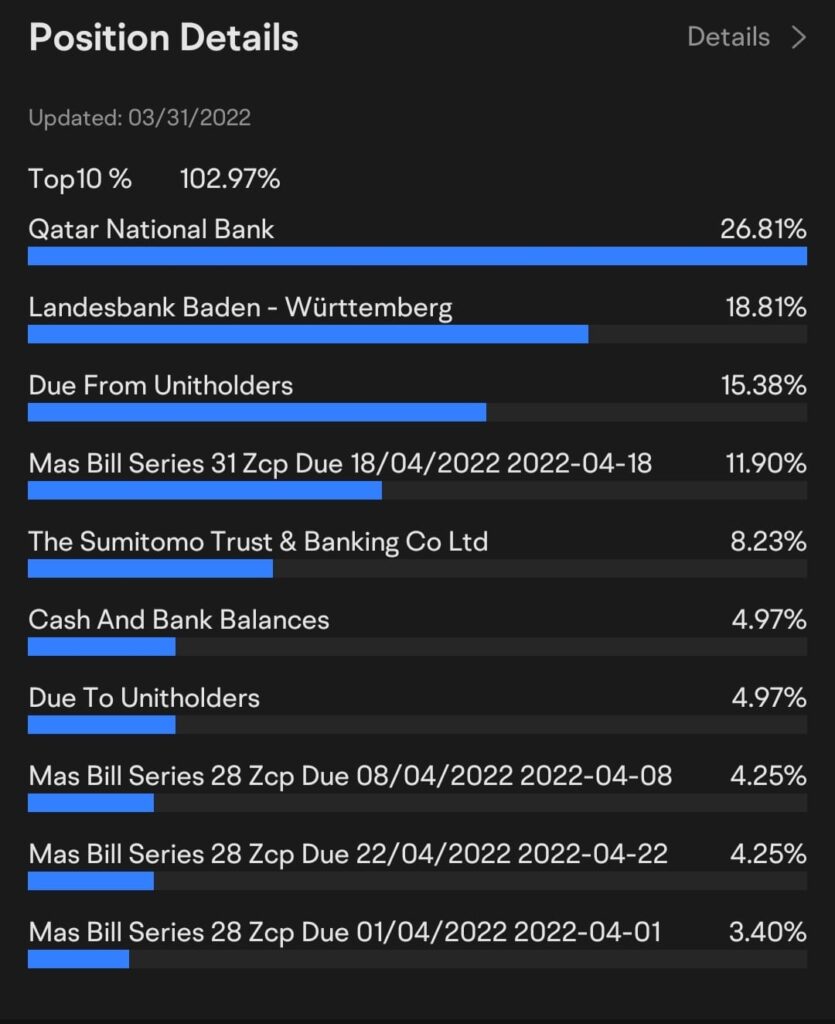

One of the engaging money administration funds obtainable to Singaporeans is the Fullerton SGD Money Fund, which is the biggest home money fund right here and with a confirmed observe file of getting constantly crushed its benchmark since its inception in 2009. Regardless of the danger of value volatility, the fund has by no means had a unfavorable month-to-month return all through its whole working historical past.

How has it fared all through 2022 – the 12 months when progress shares crashed and of Fed price hikes? It held up nicely, as you may see:

Why was this so? The reply may be present in its holdings, because the Fullerton SGD Money Fund primarily invests in short-term Singapore-dollar deposits with respected monetary establishments. For many who perceive scores, you’ll be happy to notice that these are solely devices with a minimal score of F-2 by Fitch, P-2 by Moody’s or A-2 by Customary and Poor’s.

Sadly, retail buyers can’t purchase this fund straight – however moomoo has modified this by providing people such as you and me a straightforward technique to invest in the Fullerton SGD Cash Fund – via its moomoo Cash Plus.

And should you’re searching for a USD-based money administration fund as a substitute, check out if the CSOP USD MMF would suit your wants higher.

Who’s appropriate for T-bills vs. Money Administration Funds?

There are just a few important teams of people that can be appropriate for such devices, and I’ve categorized it under:

T-bills

- Novices who don’t know easy methods to make investments, and are dissatisfied with their present financial savings returns

- Conservative people who need a secure funding / almost-zero danger choices

- Buyers who need one thing backed by the Singapore authorities

- Buyers who don’t want the money within the subsequent 6 – 12 months

Money Administration Funds

- Novices who don’t know easy methods to make investments, and are dissatisfied with their present financial savings returns

- People who need low-risk choices, and with out the excessive volatility of equities or foreign exchange

- Buyers who need to reserve the choice of withdrawing their money at any time with zero penalties

- Seasoned buyers who’re searching for a versatile place to quickly maintain their warchest money, whereas ready for alternatives within the inventory market to seem

To search out out extra about cash management funds like moomoo Cash Plus, check out this article here, the place I dive right into a extra detailed assessment of how they work and what it’s good to know.

And should you’ve all the time been somebody with spare money who solely checked out mounted deposits, try T-bills and/or money administration funds as a substitute – you may simply discover that they’re a greater, extra rewarding possibility for you.

Essential be aware: Money administration funds like moomoo Money Plus are NOT the identical as T-bills, and their core variations have been outlined on this article. Every instrument has its execs and cons, and it’s your accountability to do your individual due diligence additional earlier than deciding what to do together with your cash.

Message from our Sponsor Begin investing in funds from S$0.01, with the pliability to withdraw anytime you need to. With $0 fee, no charges for fund subscription and redemption and $0 platform charges, choose moomoo to help you start your fund investments easily today!

The moomoo app is an award-winning buying and selling platform supplied by Moomoo Applied sciences Inc., a subsidiary of Futu Holdings Restricted (NASDAQ:FUTU) and backed by Tencent. Moomoo Monetary Singapore Pte. Ltd. is regulated by the Financial Authority of Singapore and is the primary digital brokerage to have acquired all 5 memberships from the SGX Group for the securities and derivatives markets.

Disclosure: This put up is delivered to you at the side of moomoo SG. All views expressed on this article are my very own unbiased opinions. Neither moomoo Singapore or its associates shall be answerable for the content material of the data supplied.

Please be happy to click on my affiliate links if you’ll like to sign up for an account!

This commercial has not been reviewed by the Financial Authority of Singapore.

{kind=link}