What a distinction a 12 months makes! It has been only one 12 months since I last revised my article on Baby Bonus benefits and a comparison of which Child Development Account (CDA) was best to go with, and that was back in 2021 as we prepared for the birth of our second child.

And but, in a single 12 months alone, our world has ushered in an period of upper rates of interest and inflation. Many of the native banks have additionally been maintaining, and rewarding customers who proceed to financial institution and spend with them by growing the rates of interest on high-yield curiosity financial savings accounts. I used to be thus curious, what about for the children, significantly on the Baby Improvement Account the place we don’t spend as a lot or as incessantly on?

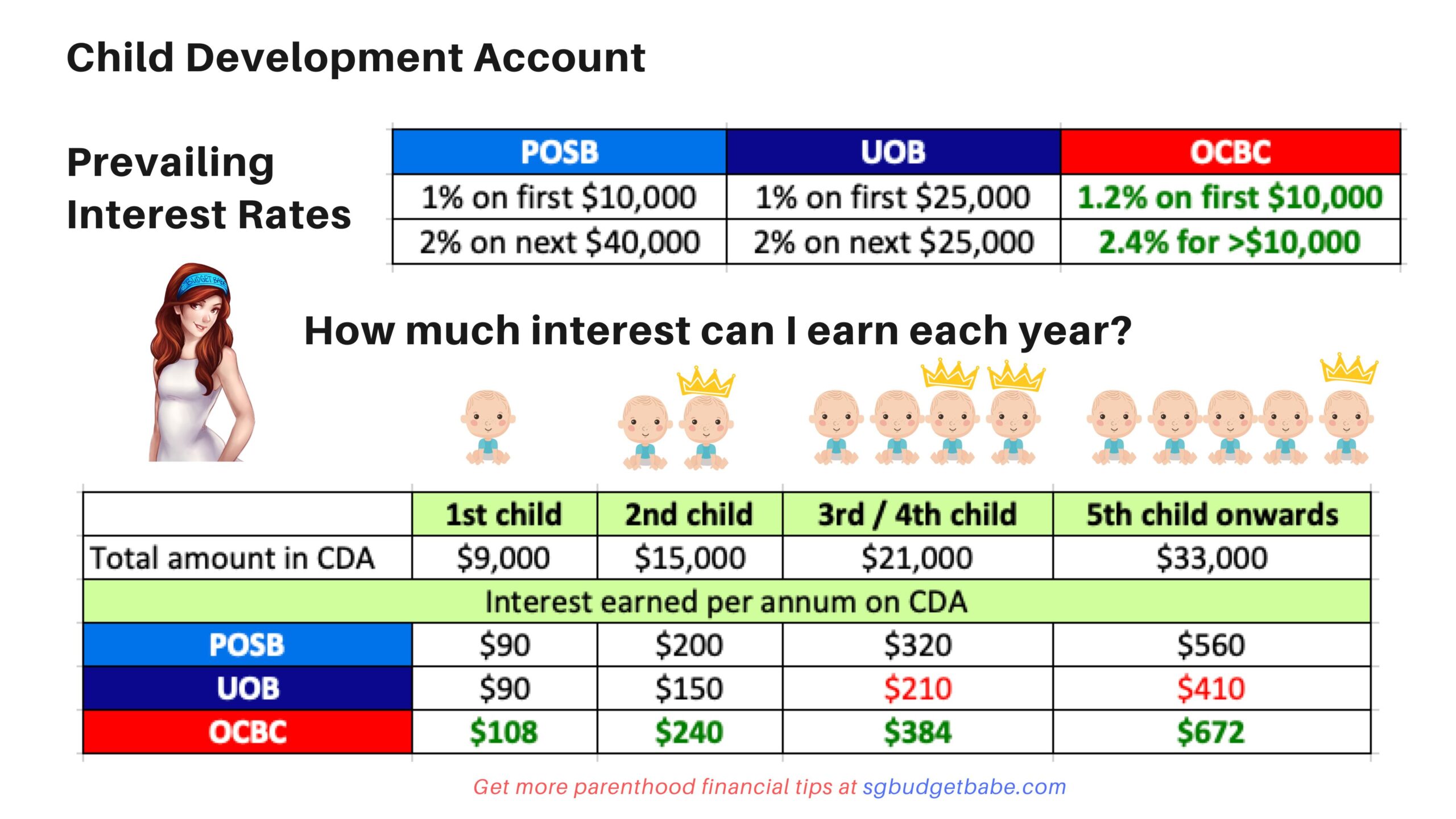

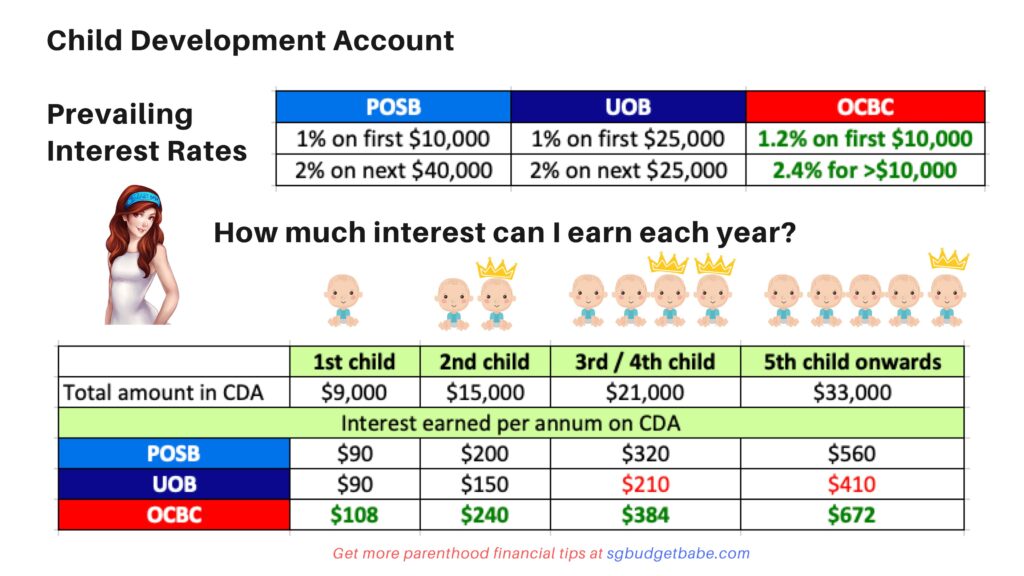

Because it turned out, OCBC is the one financial institution to have raised their rates of interest to this point. From being the worst to open your little one’s CDA account with in 2021 (given their rates of 0.6% – 0.8% back then, as captured here), OCBC is now formally the greatest CDA account to open should you’re taking a look at present charges.

In fact, there’s a catch. Not like your individual high-yield financial savings account(s), dad and mom can not merely change their little one’s CDA supplier at whim; it could solely be closed when authorities directions are acquired.

Therefore, it will be important that you simply go along with a financial institution that may hopefully decrease your regrets in a while, even when charges change. Going with the financial institution that provides the best fee proper now is probably not the case a number of years down the highway, however should you go along with a financial institution that is still aggressive and ideally truthful to customers, then your possibilities of remorse are a minimum of minimized.

You possibly can read my original post here (published back in 2018, while researching for my first child) on how we determined to go along with POSB then due to the free SIA toddler ticket (which we used for a household journey to Australia) and the assorted service provider promotions.

In 2021 when my second little one was born, we decided to go with POSB still regardless of not getting the free air ticket anymore, as a result of it will make it simpler for me to handle each their accounts (since I can entry from a single iBanking login), and the service provider promotions had been nonetheless superior by way of what appealed to us. On the similar time, POSB’s charges had been additionally the best final 12 months after we opened the account.

When you’re studying this submit in finish 2022 or 2023 and considering of which account to open, you have got a tougher option to make as a result of OCBC has now caught up and is formally the CDA supplier with the best charges available in the market proper now. We don’t know but if the opposite 2 banks will regulate their charges anytime quickly, however regardless, it’s a must to decide based mostly on the present info you have got anyway.

If I had been in your sneakers, I might do that:

- Open with OCBC provided that I have already got an present OCBC account

- Open with OCBC whether it is on your third little one onwards, because the charges are much more rewarding at this level given the upper Child Bonus quantity that you simply get from the federal government

- Open with POSB if I have already got present POSB CDAs to handle for my different youngsters

At this level, I’m not leaning in the direction of UOB as a result of I discover their lack of service provider tie-ups unattractive, and UOB charges have historically lagged behind POSB and OCBC’s for the final 4 years while I’ve been doing these analysis for my youngsters.

How a lot did we get from the Singapore authorities for having our youngsters?

Each of our youngsters have a distinct quantity in every of their accounts by the point they every turned 1 years outdated – Nate has $9,000 whereas Finn has $15,000 (not together with curiosity payouts).

The explanation for this distinction primarily lies in the truth that our authorities boosted the CDA Authorities Co-Matching Grant in 2021 (previous to Finn’s beginning), which resulted in an additional $3,000 being matched. Since we acquired $3,000 from the COVID19 Child Assist Grant for having Finn throughout the pandemic, we merely deposited this into his CDA in order that it will get matched accordingly.

In fact, if my older son had been to someday complain that that is unfair, I’ll remind him that (i) that is simply how life works and (ii) he had an enormous 100-day and 1st 12 months birthday celebration the place he acquired a pleasant 4-digit sum in ang paos, which his youthful brother didn’t have the privilege of holding because it was throughout the pandemic’s restrictions.

As a guardian, should you’re capable of do the next steps proper from the start, you’d have set your little one up for a higher monetary security internet (a minimum of for his or her training) than everybody else:

- Open the suitable CDA account

- Deposit the utmost quantity for the CDA Authorities Co-Matching scheme

- Attempt to not contact CDA funds throughout their youthful years so that you simply enable the curiosity to roll (except you’ll be able to earn the next curiosity on the quantity elsewhere, equivalent to via investments)

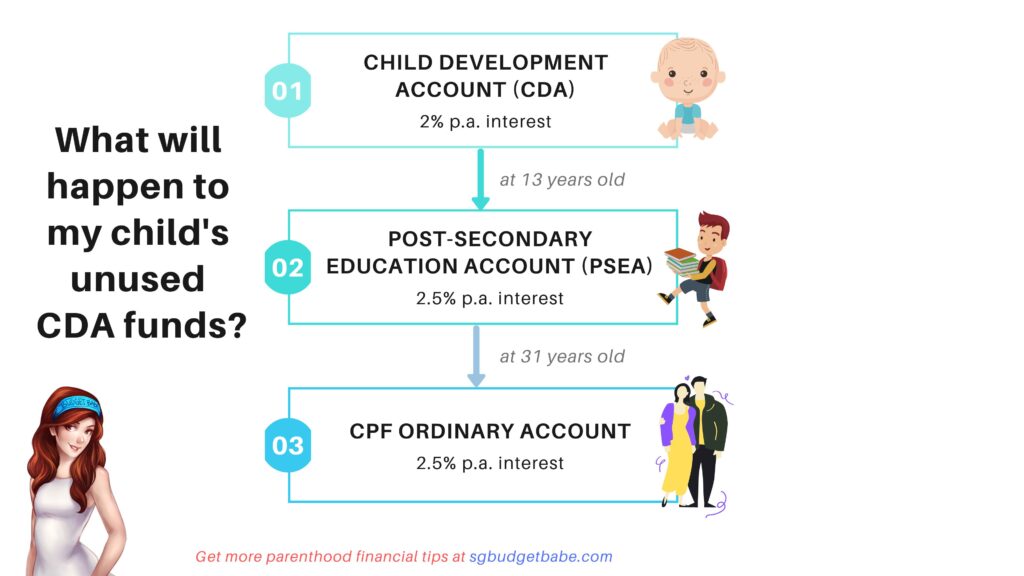

The CDA funds will circulation into your little one’s Submit-Secondary Training Account, which they will use for brief programs or workshops in a while after finishing secondary college. And if there are nonetheless any unused funds leftover, it’s going to then be credited into their CPF-OA after they flip 31 (I had $2,000+ left in mine that was credited into my CPF after I reached the age).

You should definitely begin with maximizing your little one’s CDA advantages, after which transfer on to different necessary monetary must-dos on your little one. Read the next step here.

P.S. Discovered this text helpful? Share it with a fellow guardian to assist them alongside on their parenthood journey in Singapore!

With love,

Price range Babe

{kind=link}