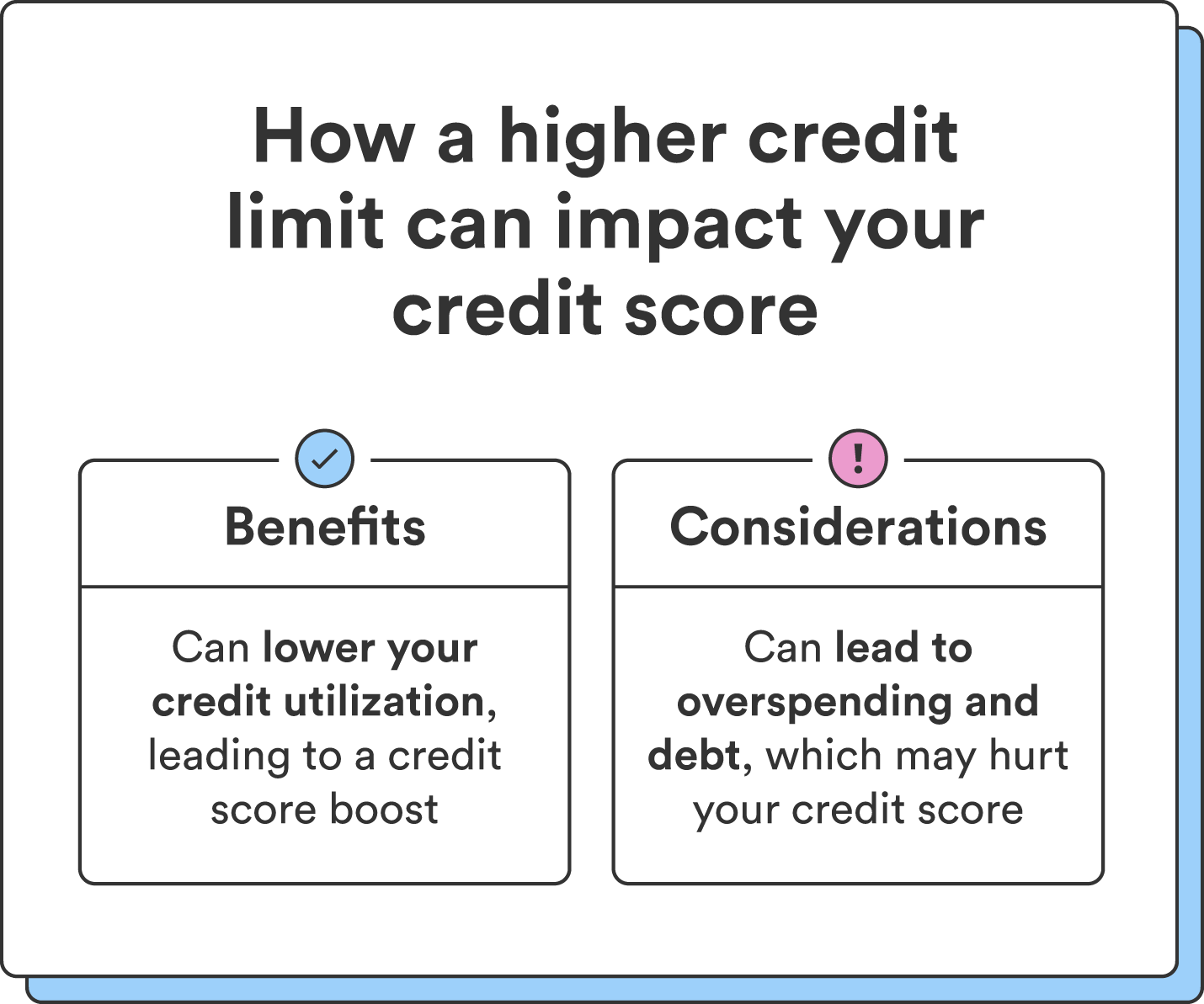

Growing your credit score restrict can each positively and negatively have an effect on your funds relying in your habits. One clear profit of a better credit score restrict is elevated monetary flexibility for surprising bills, managing debt, or making bigger purchases.

Growing your credit score restrict may also scale back your credit utilization ratio, which may enhance your credit score rating. Credit score utilization is the share of your credit score restrict that you just’re utilizing in comparison with your complete credit score restrict, and it performs a big position in your credit score rating. A decrease credit score utilization ratio is right, because it reveals you’re not overly reliant on credit score and may handle credit score responsibly.

However, a better credit score restrict can current the potential to overspend. Whereas there are advantages to an elevated credit score restrict, they solely apply should you handle your credit score responsibly. Misusing an elevated credit score restrict can result in buying extra debt than you possibly can handle, excessive curiosity prices, and monetary pressure.

Lastly, requesting a credit score restrict enhance might end in a tough inquiry in your credit report, which may influence your credit score rating. The impact of a single arduous inquiry diminishes over time and will not trigger important injury. However should you’ve already utilized for different forms of credit score within the final 12 months, your rating may drop.

Chime tip: In the event you’re planning to use for a significant mortgage, like a mortgage loan, within the close to future, keep away from a number of arduous inquiries from credit score restrict enhance requests. Credit score enhance requests may decrease your credit score rating and influence your probabilities of approval.

| Execs | Cons |

| Extra monetary flexibility | Temptation to overspend |

| Improved credit score utilization | Potential for debt |

| Potential credit score rating increase | Might include a tough credit score inquiry |

{kind=link}