Newest Updates

- Up to date with new evaluation through the Tax Basis Basic Equilibrium Mannequin.

- Up to date to replicate the newest particulars in President Biden’s FY 2025 finances.

- Initially printed following President Biden’s 2024 State of the Union Deal with.

Topline Preliminary Estimates

| 11-12 months Income (Trillions) | Lengthy-run GDP | Lengthy-Run Wages | Lengthy-Run FTE Jobs |

|---|---|---|---|

+$2.2T |

-2.2% |

-1.6% |

-788k |

Supply: Tax Basis Basic Equilibrium Mannequin, March 2024.

President Biden’s State of the Union deal with introduced a imaginative and prescient of upper taxes for American companies and excessive earners mixed with carveouts, credit, and extra advanced guidelines for taxpayers in any respect earnings ranges. Quickly after, the president launched his FY 2025 budget outlining how the White Home would implement the president’s taxA tax is a compulsory cost or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of basic authorities providers, items, and actions.

imaginative and prescient, indicating a gross tax hike of about $5.3 trillion from 2024 to 2034.

On a gross foundation, we estimate Biden’s FY 2025 finances would improve taxes by about $4.4 trillion over that interval. After taking varied credit into consideration, the rise could be about $3.4 trillion. The tax will increase would considerably improve marginal tax charges on funding, saving, and work, lowering financial output by 2.2 % in the long term, wages by 1.6 %, and employment by 788,000 full-time equal jobs.

The tax modifications Biden proposes fall underneath three primary classes: extra taxes on excessive earners, larger taxes on U.S. companies—together with growing taxes that Biden enacted with the InflationInflation is when the final value of products and providers will increase throughout the economic system, lowering the buying energy of a foreign money and the worth of sure property. The identical paycheck covers much less items, providers, and payments. It’s typically known as a “hidden tax,” because it leaves taxpayers much less well-off as a result of larger prices and “bracket creep,” whereas growing the federal government’s spending energy.

Discount Act (IRA)—and extra tax credit for a wide range of taxpayers and actions. The mixture of insurance policies would transfer the tax code additional away from simplicity, transparency, and neutrality, whereas making the U.S. economic system much less aggressive. The rise within the company tax charge and the extra taxes on prime earners would lead to U.S. prime marginal tax charges on earnings which might be among the many highest within the developed world.

Lengthy-Run Financial Results of President Biden’s FY 2025 Funds

We estimate the tax modifications within the president’s finances would scale back long-run GDP by 2.2 %, the capital inventory by 3.8 %, wages by 1.6 %, and employment by about 788,000 full-time equal jobs. The finances would lower American incomes (as measured by gross nationwide product, or GNP) by 1.9 % in the long term, reflecting offsetting results of elevated taxes and decreased deficits, as debt discount reduces curiosity funds to overseas homeowners of the nationwide debt.

Elevating the corporate income taxA company earnings tax (CIT) is levied by federal and state governments on enterprise income. Many firms should not topic to the CIT as a result of they’re taxed as pass-through businesses, with earnings reportable underneath the individual income tax.

charge to twenty-eight % is the biggest driver of the detrimental results, lowering long-run GDP by 0.9 %, the capital inventory by 1.7 %, wages by 0.8 %, and full-time equal jobs by 192,000.

Our financial estimates seemingly understate the consequences of the finances since they exclude two novel and extremely unsure but giant tax will increase on excessive earners and multinational firms, specifically a brand new minimal tax on unrealized capital positive factors and an undertaxed income rule (UTPR) in line with the OECD/G20 world minimal tax mannequin guidelines. Nor will we embody the finances’s unspecified analysis and improvement (R&D) incentives that may exchange the decrease tax charge on foreign-derived intangible earnings (FDII).

The finances would come with the next main modifications, starting in 2025, except in any other case famous.

Main enterprise provisions modeled:

- Enhance the company earnings tax charge from 21 % to twenty-eight % (efficient 2024)

- Enhance the company different minimal tax launched within the Inflation Discount Act from 15 % to 21 % (efficient 2024)

- Quadruple the inventory buyback tax applied within the Inflation Discount Act from 1 % to 4 % (efficient 2024)

- Make everlasting the surplus enterprise loss limitation for pass-through companies

- Additional restrict the deductibility of worker compensation underneath Part 162(m)

- Enhance the worldwide intangible low-taxed earnings (GILTI) tax charge from 10.5 % to 21 %, calculate the tax on a jurisdiction-by-jurisdiction foundation, and revise associated guidelines (some provisions efficient 2024)

- Repeal the decreased tax charge on foreign-derived intangible earnings (FDII)

Main particular person, capital positive factors, and estate taxAn property tax is imposed on the web worth of a person’s taxable property, after any exclusions or credits, on the time of loss of life. The tax is paid by the property itself earlier than property are distributed to heirs.

provisions modeled:

- Develop the bottom of the online funding earnings tax (NIIT) to incorporate nonpassive enterprise earnings and improve the charges for the NIIT and the extra Medicare tax to succeed in 5 % on earnings above $400,000 (efficient 2024)

- Enhance prime individual income taxA person earnings tax (or private earnings tax) is levied on the wages, salaries, investments, or different types of earnings a person or family earns. The U.S. imposes a progressive earnings tax the place charges increase with earnings. The Federal Revenue Tax was established in 1913 with the ratification of the 16th Amendment. Although barely 100 years previous, particular person earnings taxes are the largest supply of tax income within the U.S.

charge to 39.6 % on earnings above $400,000 for single filers and $450,000 for joint filers (efficient 2024) - Tax long-term capital positive factors and certified dividends at unusual earnings tax charges for taxable incomeTaxable earnings is the quantity of earnings topic to tax, after deductions and exemptions. For each people and firms, taxable earnings differs from—and is lower than—gross earnings.

above $1 million and tax unrealized capital positive factors at loss of life above a $5 million exemption ($10 million for joint filers) - Restrict retirement account contributions for high-income taxpayers with giant particular person retirement account (IRA) balances

- Tighten guidelines associated to the property tax

- Tax carried curiosity as unusual earnings for individuals incomes greater than $400,000

- Restrict 1031 like-kind exchanges to $500,000 in positive factors

Main tax creditA tax credit score is a provision that reduces a taxpayer’s ultimate tax invoice, dollar-for-dollar. A tax credit score differs from deductions and exemptions, which scale back taxable earnings, somewhat than the taxpayer’s tax invoice straight.

provisions modeled:

- Prolong the American Rescue Plan Act (ARPA) baby tax credit score (CTC) by 2025 and make the CTC totally refundable on a everlasting foundation (efficient 2024)

- Completely prolong the ARPA earned earnings tax credit score (EITC) enlargement for staff with out qualifying youngsters (efficient 2024)

We additionally modeled varied miscellaneous provisions for firms, pass-through companies, and people, together with a number of energy-related tax hikes largely pertaining to fossil gas manufacturing. Whereas the finances improperly characterizes fossil gas provisions as subsidies, many are deductions for prices (or approximations of prices) incurred.

Main provisions not modeled:

- Repeal the bottom erosion and anti-abuse tax (BEAT) and exchange it with an undertaxed income rule (UTPR) in line with the OECD/G20 world minimal tax mannequin guidelines

- Change FDII with unspecified R&D incentives

- Create a 25 % “billionaire minimal tax” to tax unrealized capital positive factors of high-net-worth taxpayers

- Completely prolong the ARPA premium tax credit (PTCs) enlargement (we do embody PTCs in our distributional evaluation)

- Develop federal guidelines on drug pricing provisions

- Spending program modifications

- Present extra Inside Income Service (IRS) funding

Income Results of President Biden’s FY 2025 Funds

The finances covers the 10-year interval from 2025 by 2034, but additionally proposes tax will increase and credit beginning in 2024. As such, we current a income desk under that features the income change over the normal 10-year finances window and the complete 11-year interval together with 2024. We seek advice from the rating over the complete 11-year interval all through.

Throughout the foremost provisions modeled by Tax Basis, we estimate the finances raises $2.2 trillion of tax income from firms and $1.4 trillion from people from 2024 by 2034. We relied on estimates from the White Home Workplace of Administration and Funds (OMB) for provisions we didn’t mannequin, together with the billionaire minimal tax, UTPR, varied worldwide tax modifications for oil and gasoline firms, smaller worldwide tax modifications, enhancements to tax compliance and administration, and unspecified R&D incentives to switch FDII.

In complete, accounting for all provisions, together with these estimated by OMB, we estimate the finances raises practically $4.4 trillion in gross income from tax modifications over the 11-year finances window.

Expanded tax credit and the unspecified incentive to switch FDII scale back the gross income by $876 billion and $118 billion, leading to a internet tax improve of $3.4 trillion.

Exterior of tax modifications, the finances contains extra spending will increase and value financial savings together with increasing the drug pricing provisions handed within the Inflation Discount Act for a internet improve in spending of $1.2 trillion, summarized in Desk 3.

After accounting for all modifications in income and spending, we estimate the online impact of the finances could be to scale back the deficit by practically $2.2 trillion by 2034 on a standard foundation. On a dynamic foundation, factoring in decreased tax revenues ensuing from the smaller economic system, the deficit discount drops to $1.4 trillion.

Nonetheless, the projected lower in finances deficits is very unsure. About $742 billion of the elevated income comes from untested sources—the 25 % minimal tax on excessive earners and the UTPR.

The 25 % minimal tax on unrealized capital positive factors has a number of novel options and would for the primary time try to gather tax on a broad set of property on a mark-to-market foundation or on imputed returns, i.e., with no clear market transaction to firmly set up any capital acquire or loss. It could apply to taxpayers with wealth higher than $100 million, requiring a brand new annual wealth reporting system.

It’s unclear what number of taxpayers could be topic to the reporting necessities and answerable for the tax, or how taxpayers would react to such a regime. Primarily based on the OMB estimate (transformed to calendar years), the minimal tax would increase about $517 billion, although it’s unclear what OMB assumed concerning avoidance conduct, valuation disputes, and different elements that would dramatically change this end result.

One other extremely unsure minimal tax proposed within the finances is a UTPR and different provisions meant to align with the OECD/G20 world minimal tax mannequin guidelines relevant to company income earned internationally. Several countries are within the strategy of implementing world minimal tax guidelines together with a UTPR, although our analysis and that of the Joint Committee on Taxation (JCT) point out a substantial amount of uncertainty in forecasting how the principles will finally evolve throughout the globe.

Moreover, the JCT finds a lot uncertainty in estimating income results of a possible UTPR within the U.S., starting from a lack of $57 billion over a decade to a acquire of $237 billion, relying on how different nations implement their guidelines. The OMB estimates the UTPR would increase about $140 billion over the finances window, which is a few quarter of what was predicted in final 12 months’s finances. OMB estimates one other $85 billion would come from disallowing overseas tax credit for oil and gasoline firms and different sundry tax will increase.

The finances discusses extra insurance policies that may considerably scale back income, akin to extending tax modifications from the Tax Cuts and Jobs Act (TCJA) for individuals making under $400,000 after 2025 after they in any other case expire. The finances doesn’t, nonetheless, think about the price of such an extension. Equally, the finances extends the bigger CTC by 2025, however additional extending the coverage would value greater than $130 billion per 12 months, including greater than $1 trillion to the deficit by 2033. Persevering with each of the insurance policies previous 2025 would wipe out most, if not all, of the finances’s projected deficit financial savings.

Distributional Results of President Biden’s FY 2025 Funds

The finances would increase marginal earnings tax charges confronted by larger earners and firms whereas increasing tax credit for lower-income households. Our modeling of the distributional results on after-tax incomeAfter-tax earnings is the online quantity of earnings accessible to speculate, save, or devour after federal, state, and withholding taxes have been utilized—your disposable earnings. Corporations and, to a lesser extent, people, make financial selections in mild of how they’ll greatest maximize after-tax earnings.

doesn’t embody the influence of drug pricing provisions, the 25 % billionaire minimal tax, the undertaxed income rule, miscellaneous tax credit, IRS enforcement, or spending program modifications.

The finances would redistribute earnings from excessive earners to low earners. The underside 60 % of earners would see will increase in after-tax earnings in 2025, whereas the highest 40 % of earners would see decreases. After-tax earnings for the underside quintile would improve by 16.1 %, largely from expanded tax credit. In distinction, the highest 1 % of earners would expertise a 8.7 % lower in after-tax earnings.

After the expanded CTC expires, the underside quintile would see a smaller 5.8 % improve in after-tax earnings in 2034 on a standard foundation whereas the highest three quintiles would see decreases of their after-tax incomes. The highest 1 % would see a 6.5 % lower in after-tax earnings.

On a long-term dynamic foundation, the smaller economic system reduces after-tax incomes relative to the standard evaluation. On common, tax filers within the prime 4 quintiles would expertise a drop in after-tax incomes, whereas the underside quintile would nonetheless see a rise, albeit decreased to three.7 %, pushed by the everlasting modifications to the CTC, EITC, and PTC.

Prime Tax Charges Underneath President Biden’s FY 2025 Funds

President Biden’s finances proposals would increase prime tax charges on company earnings, capital positive factors earnings, and particular person earnings to ranges which might be out of step with the remainder of the world.

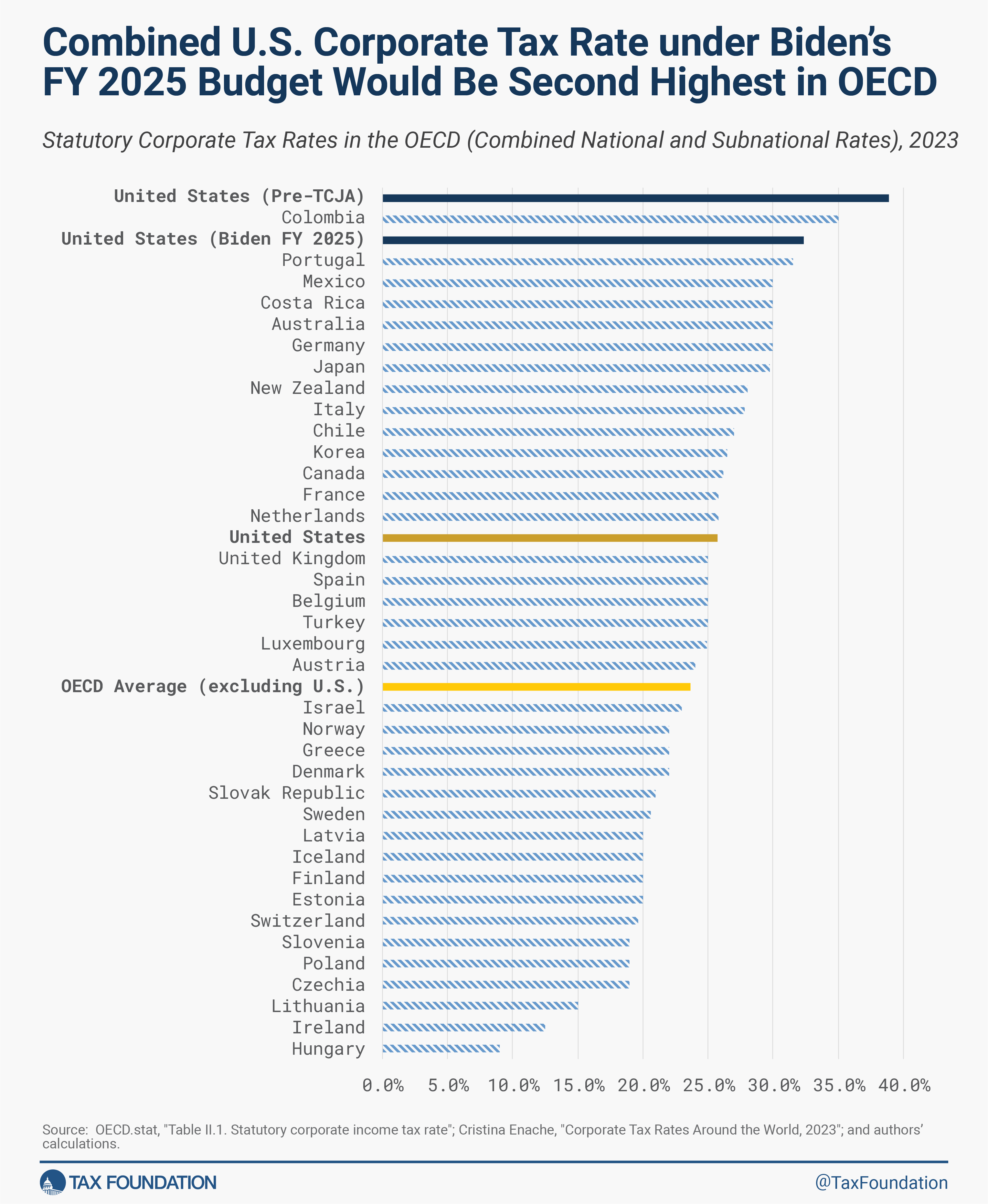

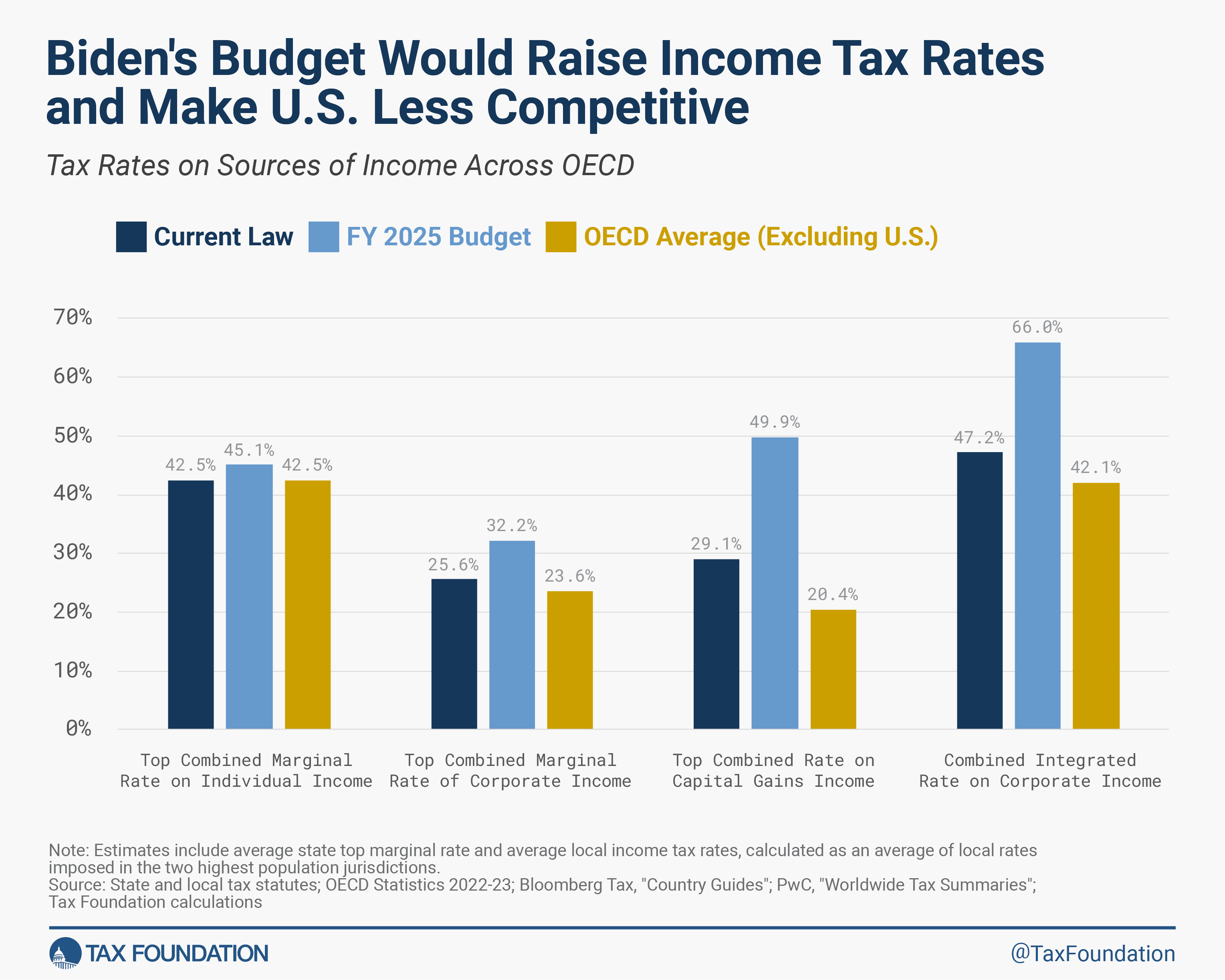

Elevating the company earnings tax charges from 21 % to twenty-eight %, a coverage Biden has pushed for for the reason that 2020 marketing campaign, would considerably worsen the aggressive place of U.S. companies and scale back prospects for enterprise funding and staff. Together with the common of state charges, the highest mixed marginal charge on company earnings underneath present regulation is 25.6 %, and Biden’s proposal would improve it to 32.2 %—the second highest company tax charge within the OECD (behind Colombia at 35 %).

The company earnings tax is probably the most dangerous tax for financial progress and its many issues have led nations all over the world to scale back company tax charges significantly over the past 40 years to a median of about 23 percent as of 2023. The U.S. had the very best company tax charge within the OECD previous to the TCJA, which lowered the U.S. company tax charge to be roughly common amongst OECD nations. Current research have decided that decreasing the company tax charge significantly boosted funding within the United States, a long-term course of that continues to yield financial advantages, together with positive factors in staff’ wages.

On prime of a better statutory company tax charge, Biden has proposed growing the speed of the brand new corporate alternative minimum tax on book incomeE book earnings is the quantity of earnings firms publicly report on their monetary statements to shareholders. This measure is helpful for assessing the monetary well being of a enterprise however typically doesn’t replicate financial actuality and may end up in a agency showing worthwhile whereas paying little or no earnings tax.

from 15 % to 21 %. The tax was enacted in August 2022 as a part of the IRA and scheduled to enter impact beginning in 2023, however the IRS postponed its implementation due to the complexity of enforcing it. Taxpayers are nonetheless awaiting steering on a number of vital questions associated to the CAMT, and it stays questionable whether or not the tax is even possible. It has definitely failed so far as an efficient minimal tax.

Biden additionally proposes quadrupling the IRA’s 1 % excise taxAn excise tax is a tax imposed on a selected good or exercise. Excise taxes are generally levied on cigarettes, alcoholic drinks, soda, gasoline, insurance coverage premiums, amusement actions, and betting, and sometimes make up a comparatively small and unstable portion of state and native and, to a lesser extent, federal tax collections.

on inventory buybacks. Inventory buybacks are one of many methods companies return worth to their shareholders. Corporations can return earnings to shareholders by issuing dividends (specifically money funds) or with inventory buybacks (buying shares of their very own firm). As much as 95 percent of the cash returned to shareholders from inventory buybacks subsequently will get reinvested in different public firms. Quadrupling the tax charge would seemingly discourage companies from pursuing inventory buybacks, probably tilting towards extra dividend issuances as an alternative, and will discourage funding.

On private earnings taxes, too, the Biden finances proposals would additional push up marginal tax charges. Underneath present regulation, the highest mixed marginal tax rateThe marginal tax charge is the quantity of extra tax paid for each extra greenback earned as earnings. The typical tax charge is the full tax paid divided by complete earnings earned. A ten % marginal tax charge implies that 10 cents of each subsequent greenback earned could be taken as tax.

on particular person earnings is 42.5 %, consisting of the highest federal charge (37 %) and the common of state and native earnings tax charges. Biden’s proposal would increase it to 45.1 % by growing the highest charge from 37 % to 39.6 %. The speed ignores the 5 % extra Medicare tax, half of which falls on the employer, as a way to make comparisons to the non-public earnings tax regimes within the OECD database. Together with the employee-side portion of this tax would increase the highest charge to 47.6 %.

Within the case of capital positive factors taxes specifically, the modifications would push america past worldwide norms. The highest mixed marginal tax charge on capital positive factors earnings underneath present regulation is 29.1 %, consisting of the 20 % capital gains taxA capital positive factors tax is levied on the revenue made out of promoting an asset and is commonly along with company earnings taxes, regularly leading to double taxation. These taxes create a bias towards saving, resulting in a decrease stage of nationwide earnings by encouraging current consumption over funding.

charge, the three.8 % internet funding earnings tax (NIIT), and the common of state and native earnings tax charges on capital positive factors. By taxing excessive earners’ capitals positive factors as unusual earnings and elevating the NIIT to five %, Biden’s proposals would increase the highest tax charge on capital positive factors to 49.9 %—the very best within the OECD.

Aiming to deal with Medicare’s rising budgetary shortfalls, the president would increase the hospital insurance coverage (HI) payroll taxA payroll tax is a tax paid on the wages and salaries of workers to finance social insurance coverage packages like Social Safety, Medicare, and unemployment insurance coverage. Payroll taxes are social insurance coverage taxes that comprise 24.8 % of mixed federal, state, and native authorities income, the second largest supply of that mixed tax income.

for individuals incomes greater than $400,000 from 0.9 % to 2.1 %, develop the bottom of the NIIT to incorporate energetic enterprise earnings, and lift the NIIT to five % for top earners. The modifications would increase prime tax charges on labor, funding, and enterprise earnings whereas not doing enough to place entitlements on a path towards solvency.

The mixed built-in charge on company earnings displays the 2 layers of tax company earnings faces: first on the entity stage by company taxes and once more on the shareholder stage by capital positive factors and dividends taxes. Underneath present regulation, the highest mixed built-in tax charge on company earnings distributed as capital positive factors is 47.2 %. Underneath Biden’s proposals, it will rise to a jaw-dropping 66 %—the very best within the OECD.

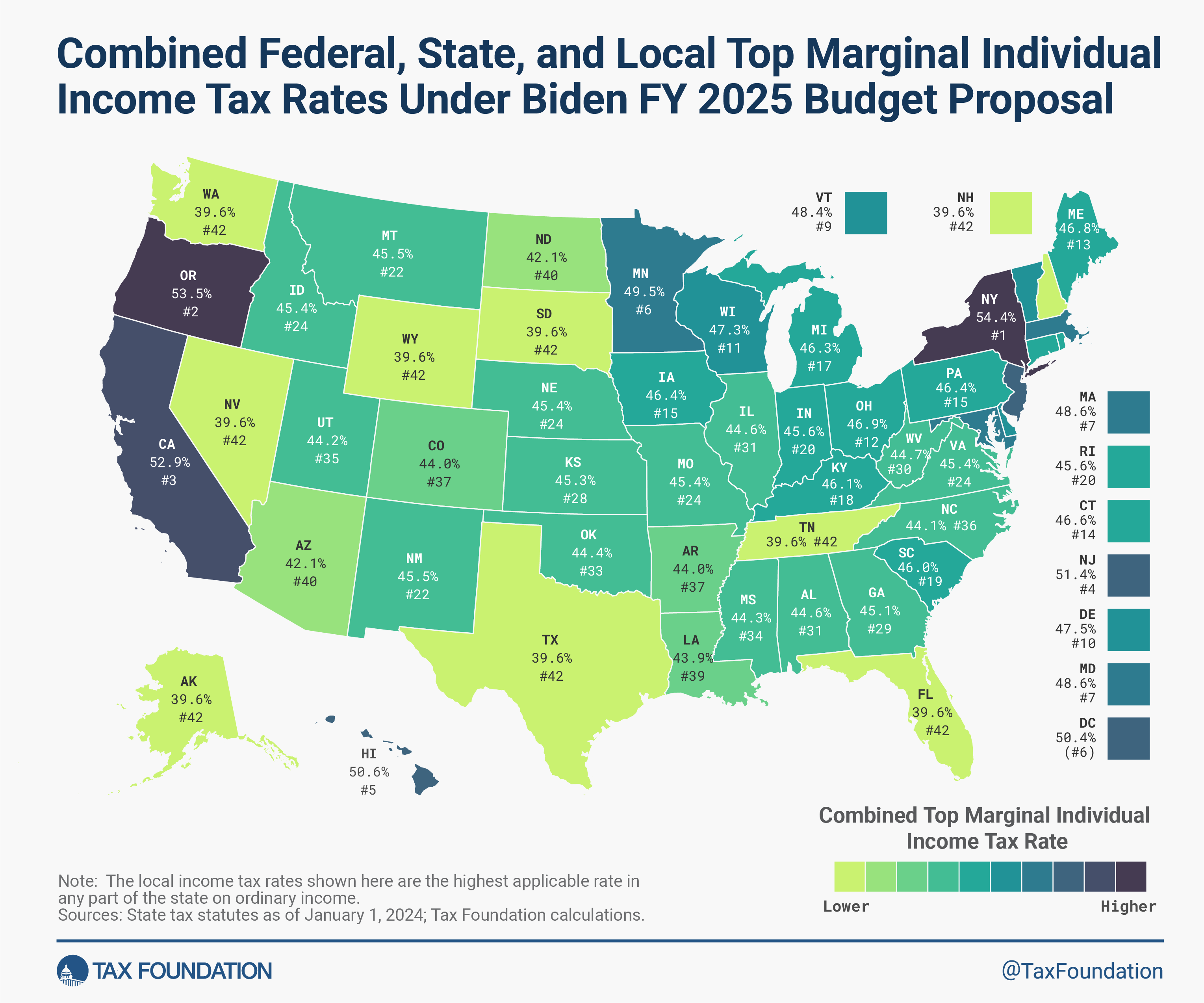

Biden’s FY 2025 finances would yield mixed prime marginal charges on particular person earnings in extra of fifty % in 5 states and D.C.: New York (54.4 %), Oregon (53.5 %), California (52.9 %), New Jersey (51.4 %), Hawaii (50.4 %), and D.C. (50.4 %).

Moreover, President Biden reintroduced his proposal to boost the efficient tax charges paid by households with internet price over $100 million. The proposal requires excessive internet price households to pay a 25 % minimal tax charge on an expanded definition of earnings that features unrealized capital positive factors. Underneath the minimal tax, households would pay tax on capital positive factors even when the underlying asset has not but been bought, working as a prepayment for future capital positive factors tax legal responsibility.

The billionaire minimal tax, as it’s generally identified, would improve the complexity of the tax code by utilizing a non-traditional and difficult-to-measure definition of earnings. It could require formulaic guidelines for valuing several types of property, cost intervals that fluctuate by asset sort, and a separate tax system to take care of illiquid property. This tax design goes properly past worldwide norms, the place capital positive factors are taxed when realized and at lower rates than the U.S. in lots of instances.

Biden would additionally develop the disallowance of deductions for worker compensation above $1 million (Part 162m) to cowl all workers of C firms. The cap at the moment applies to the CEO, CFO, and the following three highest-paid workers of an organization, and as a result of ARPA is already scheduled to develop to the following 5 extra highest-paid workers starting after 2026.

Increasing the disallowance makes it costlier for firms to draw and retain prime expertise. It could imply each the company and particular person prime tax charges would apply to wages, leading to prime tax charges of 70 % or extra together with state taxes. If the $1 million threshold will not be listed to inflation, over time the tax would hit extra than simply the C-suite.

Different Provisions

In search of to deal with the very actual downside of housing affordability, Biden has referred to as for a number of proposals to subsidize residence purchases and increase the low-income housing tax credit score, together with a tax credit score price $5,000 per 12 months for two years for middle-class, first-time homebuyers. The president would additionally supply a one-year tax credit score price as much as $10,000 for middle-class households who promote a starter residence to assist enhance starter residence availability. Lastly, the president proposes to offer as much as $25,000 in down cost help for first-generation homebuyers.

Boosting demand by subsidies is more likely to trigger housing costs to extend additional. What is required is a higher provide of housing, which might be greatest completed on the state and native stage by reforming zoning guidelines and on the federal stage by reforming tax depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, akin to equipment or a manufacturing facility, to find out the multiyear interval over which the price of that asset may be deducted from taxable income. As a substitute of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, lowering their worth and discouraging funding.

guidelines for residential structures.

For builders, the president would develop the low-income housing tax credit score (LIHTC) and create a brand new neighborhood houses tax credit score to construct or renovate reasonably priced homes. This strategy could be an inefficient solution to construct new houses as the present LIHTC is expensive for the houses produced, with a lot of the credit score worth going to developers and financing agencies.

President Biden would renew the expanded baby tax credit score from the 2021 American Rescue Plan Act, which might increase the CTC worth from $2,000 to a most worth of $3,600 whereas eradicating work and earnings necessities. This CTC enlargement would have main fiscal prices totaling over $1 trillion over 10 years above the current-policy CTC. If we embody the underlying CTC enlargement from the Tax Cuts and Jobs Act that expires at the end of 2025, the associated fee approaches $2 trillion over 10 years.

Along with the CTC enlargement, the president would develop the EITC and make everlasting the expanded Reasonably priced Care Act (ACA) premium tax credit which might be scheduled to run out on the finish of 2025.

President Biden additionally dedicated to preserving and lengthening the additional funding appropriated to the IRS as a part of the Inflation Discount Act. Biden argues this might assist increase income from larger earners who evade taxes and would additionally enhance taxpayer providers. A lot of this new income could take time to seem because the IRS trains new workers and spends time figuring out evasion and implementing the tax regulation. Nonetheless, the opposite parts of Biden’s tax plan will push the code in a extra advanced path, making the job of the IRS to implement the regulation harder.

Lastly, the president recommitted to not elevating taxes on individuals incomes underneath $400,000, arguing that he would totally pay for expiring TCJA particular person tax modifications with “additional reforms” that may additional increase taxes on excessive earners and companies. The unspecified reforms would want to complete at least $1.4 trillion to cowl TCJA extension for individuals incomes underneath $400,000.

Conclusion

The president’s tax coverage proposals as outlined within the State of the Union deal with would make the tax code extra difficult, unstable, and anti-growth, whereas additionally increasing the quantity of spending within the tax code for a wide range of coverage objectives not associated to income assortment.

We estimate the proposed finances would scale back deficits by $1.4 trillion on a dynamic foundation by 2034 in comparison with the White Home estimate of $3.2 trillion. Nonetheless, neither estimate contains the price of the meant extension of the TCJA tax cuts for individuals incomes lower than $400,000 or for the proposed expanded CTC post-2025, which might wipe out a lot of the touted deficit discount.

The finances additionally assumes an unrealistically excessive charge of progress within the economic system, particularly contemplating the massive tax will increase proposed on companies and excessive earners that may gradual progress. The finances assumes actual GDP will develop at 2.2 % yearly within the final 5 years of the finances window, whereas the CBO assumes actual GDP will develop about 1.9 % yearly over this era. By elevating marginal tax charges on funding, saving, and work, we discover Biden’s FY 2025 finances would scale back long-run financial output by 2.2 %, wages by 1.6 %, and employment by 788,000 full-time equal jobs.

In sum, President Biden is proposing terribly giant tax hikes on companies and the highest 1 % of earners that may put the U.S. in a distinctly uncompetitive worldwide place and threaten the well being of the U.S. economic system. The finances ignores or makes unrealistic assumptions concerning the fiscal value of main proposals in addition to financial progress underneath larger marginal tax charges on work and funding, concealing what’s more likely to be a considerable value borne by American staff and taxpayers.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

Modeling Notes

We use the Tax Basis General Equilibrium Tax Model to estimate the influence of tax insurance policies, together with current updates permitting detailed modeling of U.S. multinational enterprises. The mannequin produces typical and dynamic income and distributional estimates of tax coverage. Standard estimates maintain the dimensions of the economic system fixed and try to estimate potential behavioral results of tax coverage. Dynamic income estimates take into account each behavioral and macroeconomic results of tax coverage on income. The mannequin additionally produces estimates of how insurance policies influence measures of financial efficiency akin to GDP, GNP, wages, employment, capital inventory, funding, consumption, saving, and the commerce deficit.

Notice, nonetheless, our typical and dynamic estimates for the inventory buyback tax don’t account for behavioral shifting from buybacks to dividends, which might additionally shift the person earnings tax baseThe tax base is the full quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slender tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges.

from capital positive factors to dividends.

Relating to the finances’s proposed modifications to the GILTI regime, we modeled a lot of the main modifications together with the 75 % GILTI inclusion charge, country-by-country software, the discount within the overseas tax credit score (FTC) haircut to five %, elimination of the certified enterprise asset funding (QBAI) exemption, and elimination of the FOGEI exclusion. We didn’t mannequin the modifications permitting carryforward of GILTI FTCs and losses, repeal of the high-tax exemptionA tax exemption excludes sure earnings, income, and even taxpayers from tax altogether. For instance, nonprofits that fulfill sure necessities are granted tax-exempt standing by the Inside Income Service (IRS), stopping them from having to pay earnings tax.

for subpart F, or the tax will increase on twin capability taxpayers.

Share

{kind=link}